British Farming's Stuttering Automation Drive

The beleaguered sector will need to automate heavily to secure its long term future. In light of uncertainty and high energy prices, its ability to achieve this is in doubt.

Source: WSJ

Clarkson’s Farm may have kindled public endearment towards farming. But in modern economic thinking, agriculture is almost as low-status as petrochemicals. Though politically perilous, the decline in a country’s agriculture is not generally considered a portent of wider economic malaise. Having agriculture as a more minor part of the overall GDP is generally perceived as a good thing. While valid globally, the UK’s agricultural sector is diminutive even when matched up against comparable countries. Agriculture as a percentage of GDP for the UK is 0.7%. For Germany it is 0.9%, the U.S. 1%, Sweden 1.3%, Holland 1.5%, France 1.6%, and Australia 2.3%.

Picture 1: Source: USDA

British farming revenue has hovered at around £6 billion since 2011, with considerable declines between then and now. The country’s total agricultural spending, including inputs and outputs, is around £30 billion. The country has become less self-sufficient in food production over recent years. In 2020, the production-to-supply ratio for all foods was 60%, whereas in 1989 it stood at 75%. The figures for indigenous food are 87% in 1989 and 74% in 2020. In reality, we are importing over 40% of our food as some of our produce is exported. We are nevertheless more self-sufficient than during the two world wars.

The average farm size in the UK is 70 hectares — high compared to Europe but low compared to the Americas or Australia. Across 216,00 British farm holdings, there are some 300,000 farmers and 160,000 additional employees and casual workers. One subsector is far more labour-intensive than others. Horticulture had 7.1 workers per holding in 2021, compared to 2 or fewer workers per holding for the other farm types. Around half of the horticultural workers are ‘casual’, meaning they are mostly migrant workers from overseas.

Farming is at this point low-margin and relies on subsidies. The average farm business income between 2018 and 2021 was £50,900, with as much as 54% of that being direct payments or subsidies. This varies hugely by sector. Those direct payments have been coming from the EU via the Common Agricultural Policy (CAP), but are now being filled by the government post-Brexit. From 2021-27 the Government will phase out in England the CAP-style 'direct payments' which are based on how much land is farmed. Farmers and land managers will in the future be paid to produce 'public goods’ such as environmental and animal health improvements under Environmental Land Management schemes (ELMs).

Food security is not the primary economic issue in the UK. Rather, it is the future of farming as a commercially viable sector.

The case for automation

Agriculture has been heavily mechanized in the last century. By the standards of most countries, the UK is unautomated. We have a lack of machines to complement the workforce. This extends to agriculture.

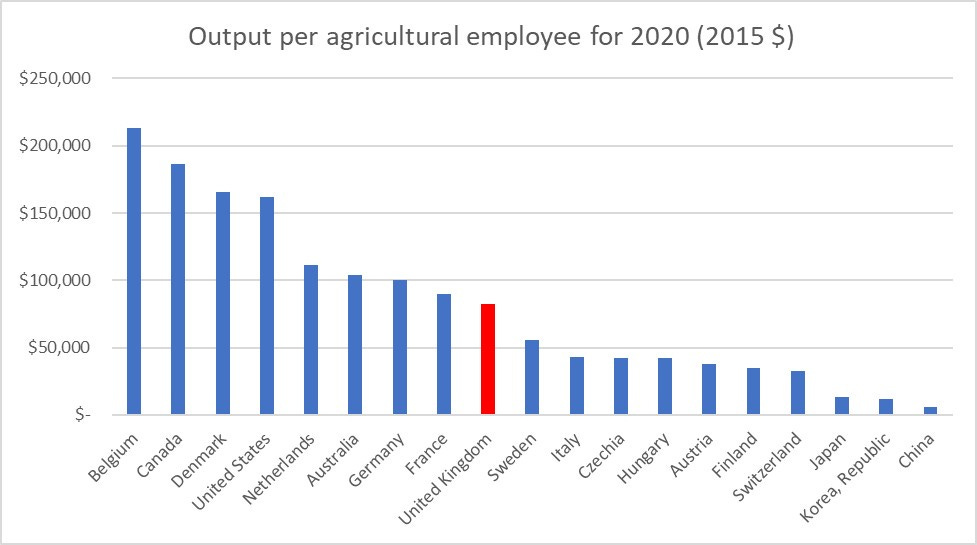

Using the excellent research service of the U.S. Department of Agriculture, we find some interesting points. First, we can see that, compared to other major economies, the UK is around average in terms of farming productivity.

Picture 2: Source: USDA

Agriculture has historically low productivity but has high productivity growth. This has been true with the UK, due to mechanization. But productivity growth has slowed markedly since 2008. Today, agriculture remains one of the least productive sectors of the UK economy. Output per worker is just £16 per hour compared to £38 for the overall economy. This is driven by the high average hours worked, labour intensity, and the relatively low price of goods. The dividend of adding more tractors, harvesters, and milking machines has petered out. UK productivity is also well behind other producers, including the U.S. and the Netherlands. By dividing a country's machinery (measured in horsepower) by the agricultural workforce, we can determine the amount of horsepower per 1,000 employees. Combining this ratio with productivity shows a clear correlation between machinery usage and higher productivity.

Picture 3: Red denotes the UK, Source: USDA

While the situation appears far from dire, British productivity is falling below that of other countries. Total factor productivity in 2020 was 93% of what it was in 2015. For Germany, it was 105%; for the U.S. and the Netherlands, it was 102%. France had a mild decline at 99%. Should the status quo continue, British farming will be in a noticeably worse place 10 years from now.

Broadly speaking, more machines will mean more productivity. Since mechanization has progressed, more productivity growth will be found in automating machinery than simply adding new hardware. British agriculture’s future is, therefore, heavily dependent on its ability to invest in and oversee greater automation.

While farming is not as critical to Britain’s long-term prosperity as other industries, its decline would have outsized effects on the country, especially in terms of regional inequality. This makes the success or failure of automation in this sector of critical importance.

Vertical farming vs Automating tractors

There are two basic forms of automation in agriculture. There is the deployment of remotely operated and automated mobile vehicles, whether that be tractors, small platforms, or drones. Then there is the capital-intensive fixed automation associated with vertical farming, exemplified by companies such as Berlin-based Infarm. Vertical farming involves growing crops on stacked layers through technologies like LED Lighting, hydroponics (artificial alternatives to soil), and monitoring sensors.

The Dutch in particular have massively expanded horticultural production over the last 30 years through indoor farming, as well as pioneering dairy milking machines. Though their machinery-to-labour ratio is lower than Britain, this is deceptive. Dutch mechanization is not measured by vehicles, but by increasingly automated greenhouses, hence it doesn’t get measured by horsepower.

Through capital investment into vertical farming and greenhouses, cheap European labour, and very cheap energy from the Groningen gas field, Holland became the second-largest exporter of food globally behind the U.S., exporting £93 billion worth in 2021. That is worth more than what the UK exports in financial services (£71 billion).

This option can pay real dividends for horticulture but is capital-intensive and energy-intensive. The UK has a £270 million farming innovation program, but such amounts are insufficient. In December 2022, a further £12.5 million in funding grants for robotics and vertical farming was provided. This was earmarked by the DEFRA secretary during a trip to Holland, where he remarked on the high level of automation in Dutch greenhouses. This was not well-received by many British horticulturalists, who argue high energy prices and lack of supply of seasonal workers are immediate challenges that will not be fixed by capital-intensive automation in the UK.

The UK does have some footprint in fixed automation for farming. Rothamstead Research, a UK-based international organization, was funded by the U.S. government and is testing the largest fixed agricultural robot in Arizona. The organization’s gantry-mounted scanalyzer is 70ft high (about 21,3m), 92ft wide (28m), and 1 200ft (366m) long, with its purpose being very discrete data collection on plants.

Picture 4: Rothamstead Research’s scanalyzer robot, the world’s largest robot

But generally speaking, our facilities are behind the continent's, and the relative energy poverty of the UK makes uptakes in such intensive infrastructure even harder to envisage.

While vertical farming is expensive and would require a major improvement in British industrial electricity prices, it is at an advanced stage of commercialization. The other type of automation, including automating outdoor farm vehicles and using robots for discrete tasks like picking fruit, is at a much more nascent stage of development.

The UK start-up scene in this space is fairly healthy, especially regarding mobile robots designed for data collection, weeding, picking, and so forth. Muddy Machines, E-Nano, and Small Robot Company are just some of the players worthy of note.

However, this form of automation is proving difficult to test and implement at scale. When talking to roboticists, the general view I got was that they did not trust robots to be on their own in the field. The propensity for things to go wrong with automated vehicles plagues the robot industry whether it's targeting tractors or commercial vacuums.

Many specialized robotic farm vehicles suffer from dubious economics. They cannot go on roads, so if they move from field to field, they must be transported. A solution is linking sensors to a regular tractor CAN bus to automate existing vehicles. These opportunities are currently large and hypothetical, and very few examples anywhere in the world of automated farm vehicles being used at scale. The technical challenge is even greater for more advanced tasks like picking fruit and crops.

With this in mind, DEFRA’s £12.5 million for robotics is not a very significant addition to funding. The government’s report on agricultural robotics argues commercialization is currently some 10 years away, and that many horticultural activities cannot be automated at the current level of progress.

Regulation

Some of the challenges of robots in farms are due to the regulatory regime.

Take the EU. The Commission’s Machinery Directive 2006/42/CE, which Britain still relies on, never refers to autonomous vehicles. The current directive demands that manual drivers control vehicles like tractors. This sounds reasonable but requires that autonomous robots have an individual supervising them even as they are driving around fields.

While onsite supervision might be reasonable for machinery that weighs over a tonne, many robots being tested on farms are much lighter, as shown below.

Picture 5: A Robot doing testing for data collection, Source: Kristof Hayes

Muddy Machines in the UK and Swarmfarm in Australia make small vehicles for whom the potential danger is less than a John Deere harvester. Currently, there is no distinction between such machines.

Interpretations of this directive mean the beyond-visual line of sight (BVLOS) standard applied to unmanned drones is also applied to ground-based robots doing seeding, harvesting, or surveying. Engineers or farmers cannot leave a robot in the field while doing something else. This significantly limits testing and eventual scale-up of the technology.

The EU is revising this machinery directive into a regulation on machinery and artificial intelligence. Depending on how intelligent a device or vehicle is deemed to be, it could require third-party certification. When initially drafted in 2021, this caused considerable opposition from the European robotics community. Whether this still affects robotics would be case-dependent. The European Agricultural Machinery Association (CEMA) has been consulting with the EU on this regulation but is irritated at the potential need for supervisory stations being needed for ground robotics operations. Experts in farming robotics expect that in 2024 the EU rules will permit offsite supervision under certain conditions, which may allay fears.

Australia has a very permissive regulatory framework for agri-bots, based on the experience of its mining companies using remotely controlled haulage vehicles in the Pilbara mines in the West of the country. There, one operator is remotely managing multiple haulage vehicles, instead of being on-site. These retrofitted Komatsu vehicles weigh 210 tonnes and can carry a further 320 tonnes of coal and debris. With minimal legislation, a similarly permissive attitude is being taken with robots in Australian agriculture.

Picture 6: Australian mining companies have been operating automated haulage vehicles since 2008, Source: Future Bridge.

In the U.S., regulation varies by state. In California, for example, the operator must be present alongside the autonomous machine to take control of it. While not an existential matter, it is no help either. Monarch, the first U.S. developer of an automated electric tractor, was ruled against by California’s health and safety authorities when asking to enable automated driving of its tractor without a human at the wheel.

Picture 7: Monarch autonomous tractor, Source: The Robot Report.

The UK, which currently relies on the Machinery Act, can take a permissive stance on mobile robots in agriculture. The seminal work on UK regulation has been a Harper Adams University study. Published in 2021, it outlines how reducing the need for direct supervision would significantly improve the economic return on automation. In 2022, this paper inspired a draft code of conduct that has been published at the British Standards Institution (BSI) which will be completed by the summer. While it would be nice to follow the Australian example, Britain is a harder place to test farming drones by default of population density. You don’t get columns of National Trust types yomping through Western Australian farmsteads.

Permissive regulation will be essential but insufficient to bring automated tractors and strawberry pickers to the UK. While drones can do imagery and analyze crop health, bringing sensors closer to and even under the soil is very valuable. The prospect of ending longstanding contentious arguments over cheap labour shortages through high-productivity machinery is enticing.

Having talked to some roboticists in this space, there is a worry that more achievable solutions like data analytics are being pursued ahead of automating manual tasks like driving or picking on the basis that they are easier. While actionable data can be valuable, farmers will want to prioritize a machine that replaces manual labour, rather than one which gives them more data to assess.

The need for cheap energy

Britain’s agricultural sector is relatively small by regional standards and is heavily reliant on imports. It is also relatively low in productivity, and high productivity growth has stagnated and even declined over the last 10 years. We rely more on cheap labour from overseas workers — particularly in horticulture. Farming is subsidized extensively by the taxpayer via the British government. With the long-term increase in energy costs due to a poorly configured grid and problems with the fertilizer supply chain, the situation is becoming more precarious.

The most notable sector is horticulture (vegetables and plants), where Britain’s trade deficit is the largest. We can look to the Dutch for some inspiration, but the primary challenge is raising sufficient capital to spend on intensive fixed automation offerings like vertical farming, as well as more experimental mobile robots for picking, weeding manipulation, data analysis, and so forth.

The current money allocated to improvements in agriculture, at around £300 million, is insufficient and needs to be raised. The rationale is more investment now will pay off in 10 years with a more productive sector that can better fulfill Britain’s calorific needs. This is unlikely to be persuasive at the Treasury for the moment.

One way to spur adoption could be revising the allocation of subsidies. The government’s current plans are to make subsidies contingent on environmental stewardship, but not on capital investment. Defra could partially index future subsidies not just to environmental stewardship, but to investments in automation. There may be a conflict here, where more productivity leads to business growth, making it harder to hit environmental targets. It would be important to assure producers’ attempts at large-scale automation are not punished.

Beyond increasing investment, there is the question of regulation. While little action is needed on fixed automation, mobile robots, whether remotely operated or automated, are at a critical stage of their adoption. Currently, regulations, especially regarding the proximity of human supervisors, are unclear and limit adoption. The wheels seem to be in motion to make them more friendly to roboticists in 2023.

Permissive regulation on supervising robots and incentives to adopt them through subsidies will help. But hanging over this is a strategic problem — the ever-rising cost of energy. In 2022, agricultural production in Lea Valley, one of Britain’s most productive horticultural hotspots, suffered as 10% of local growers ceased operations, with many blaming high and unpredictable energy costs.

After researching this issue and asking multiple experts about the outlook for robots in British farming, the general takeaway was that the industry needed predictability before any further ambitions over automation could progress. Much of the unpredictability is down to the government’s restructuring of subsidies and the potential downsides of trade liberalization. But the essential problem was the high cost of energy. Automation is, fundamentally, the substitution of human labour with mechanical, electrical, pneumatic, hydraulic, and thermal power. Hoping for widescale automation without energy abundance is likely a fool’s errand.

Availability and cost of energy is clearly a challenge for agriculture, but the nature of that challenge may vary depending on which type of agriculture. Vertical farming is more energy intensive than growing vegetables outdoors and so energy price matters for that technology regardless of the level of automation. But for arable farming, autonomous equipment does not necessarily require more energy than human operated conventional equipment and if may even be more efficient in some cases. For arable farming the bigger problem is likely to be the form of energy available. Conventional farm mechanization is designed assuming a relatively low cost source of mobile power such as diesel fuel or gasoline, but renewable energy more often is electrical. With current technology the energy density of batteries is much less than fossil fuel. In countries with large scale farming (e.g. USA, Canada, Australia, Brazil) hydrogen is a possibility, but for the UK the most likely solution is to redesign cropping practices to reduce draft power for tillage and mechanical power for on-the-go threshing in combines so that renewable electricity from wind, solar and hydro can be used. That electrical farm equipment is likely to be in the form of relatively small autonomous machines. That redesign is technically possible. Most of the component technology already exists. But the entrepreneurship and investment required to bring to market an all electric farm mechanization system could only be justified in the UK with an international market in mind.