Vassal State

Angus Hanton's screed against U.S. influence is eye-opening and worthwhile. But as befits a vassal, solutions are found wanting.

Angus Hanton’s “Vassal State”, detailing British economic subordination to the United States, is punchy, insightful, packed with interesting facts, and a welcome contribution to discussions of British political economy. His main thesis is that Britain is massively influenced by U.S. corporate power, primarily in private equity, acquisitions from large American corporations, and the scale of U.S. Big Tech. He argues that U.S. influence is disproportionate in Britain, with other countries being far more willing to challenge U.S. primacy at least as it applies to their own countries. Thirdly, he argues this is bad and can be reversed through greater cooperation with Europe.

I agree with the first point. It is undeniable that, over recent decades, U.S. primacy over Britain has extended beyond geopolitical imbalances to a more fundamental domination of British corporate and public life. The second point is true, although merely by a matter of degrees, and there are smaller countries, like Ireland, that are even more reliant on the U.S. than Britain is. The third point, that this is bad and reversible, is contestable, and limited answers are offered. This book, therefore, feels like a start to a wider discussion rather than a comprehensive plan to extricate ourselves from the Columbian yoke.

The scale of American influence

Foreigners own over 60% of British quoted shares. About half of this is owned by U.S. shareholders. This means that American ownership of British shares is an astonishing 60% of domestic ownership. Factor in the shares attributed to tax havens, which are likely stand-ins for American owners, and it is not inconceivable that, within a decade, American ownership of Britain’s open economy could eclipse domestic shareholders.

Every year, there are more acquisitions of British companies than vice versa, disproportionately from American companies. Hanton refers to Parker Hannifin’s takeover of defence contractor Meggitt. Chatting to British VCs, their main job is getting any prospective British software company to a certain level of financial attractiveness before offering them up to American buyers. The London Stock Exchange has lost value relative to the Nasdaq. Perhaps there is something that can be done about this.

Even when critiquing British governance and trying to reform our moribund economy, we find ourselves dominated by Americans. I am pro-growth and anti-declinist as the next Anglofuturism podcast guest, but it is notable how dominated by Americans this movement is. ARIA, a derivative of the American DARPA, is staffed with Americans, including the CEO. One of its board members and two of its seven advisors are current or former Google employees. Think tanks like the Social Market Foundation and Tony Blair Institute produce work in partnership with U.S. tech companies.

There are some egregious examples of contempt for Britain. For example, the U.S. embassy refuses to pay London’s congestion charge. The U.S. private equity firm HIG likely engineered the bed manufacturer Silentnight’s insolvency so it could buy it without its pension obligations, with the assistance of auditing firm KPMG. Not mentioned by Hanton is the fact the U.S. doesn’t even back Britain in international disputes. The Whitehouse does not recognise us as the rightful owners of Gibraltar, despite the fact they use it as a base. There is no sugarcoating it, in geopolitical parlance, we are a bitch.

Is Britain exceptional?

So are we exceptional? Depends on the comparison. For France, in 2023 foreigners owned 46% of listed shares, notably less than the British equivalent. Importantly, ownership was more diversified, with European shareholders having 40% of foreign ownership and Americans around 35%. While the difference may seem small, foreign ownership of French shares has remained stable at just over 50%, in large part because of foreign direct investment controls deterring foreign takeovers. The French government is a significant investor itself, having over £50 billion worth of investments in listed companies, while for Britain it is around £13 billion.

Germany is more complicated. In 2023, Germany became the top destination for inward foreign direct investment, overtaking the U.S. in real terms. A majority of DAX shares are owned by foreign investors, with most being European or American. From 2006 to 2021, institutional ownership has doubled from 21% to 40% on the DAX, and over 80% of this is foreign. Germany has definitively opened up as an economy, as evidenced by takeovers such as Chinese Midea Group’s acquisition of robotic arm maker Kuka in 2016.

The caveat to this is that listed shares are a smaller part of overall ownership in a country where family and foundation ownership is still commonplace. In 2022, the total market cap of British listed shares was 99% of GDP, while for Germany it was 45%.

Many smaller countries, including EU members, are if anything more dependent on the U.S. than Britain. In Ireland, Hanton notes that U.S. corporate sales are 200% of GDP, compared to 25% for the UK. We are arguably midway between tiny states that are U.S. clients, such as Ireland and Luxembourg, and mid-to-large European states that are nominally less exposed, such as France, Germany and Sweden.

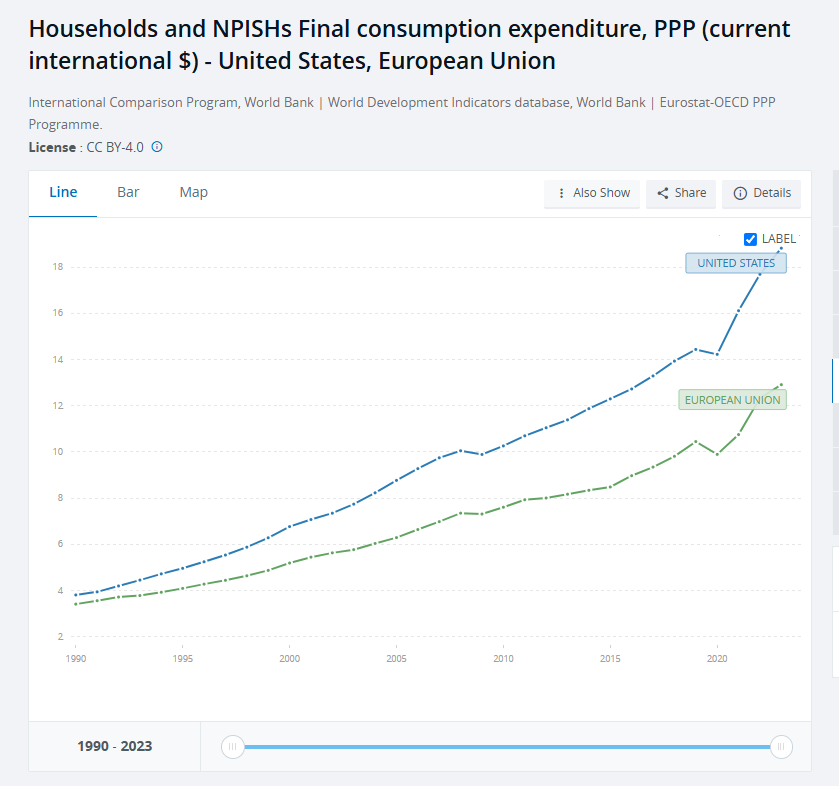

Of course, dependence on the U.S. market is hard for any European country to avoid. Though GDP shows one story, in terms of household consumption (by purchasing power parity), the U.S. is still by far the world’s largest market, over one-third larger than that of the European Union.

The U.S., because of its unique healthcare system and population, is close to 50% of the global pharmaceutical market in terms of sales. Novo Nordisk, the great exemplar of European scientific and corporate excellence, relied on North America for 61% of its 2024 sales. While the semiconductor market is seen by some as dominated by Taiwan, in reality, American companies own 50% of the market’s value. Here, Britain is not exceptional. Ineos, Britain’s great refining and chemicals conglomerate, relies on the U.S. for 70% of its profits.

Bernard Arnault, the Augustus of Veblen Goods, has relied on the U.S. investigative firm Kroll to expand his business empire. Macron has fallen back heavily on McKinsey to fill what appears to be an intellectual vacuum within his administration. While we talk about ASML as Europe’s answer to U.S. technological dominance, in reality, much of its intellectual property is owned by the U.S., hence why it can be restricted from selling its finest machines to China. Another Anglophone country, Canada, is if anything more of a U.S. vassal, being a net exporter of crude but a net importer of refined fuels.

So if Britain is one of the countries more in thrall to American power, I think this means we are just at a more advanced stage than other U.S.-aligned countries. U.S. relative decline vis-à-vis China for the last few decades has been countered by relative growth over Europe and, to an extent, the developed East-Asian world. This is down to better economic performance due to strong fundamentals like cheap energy but also a much looser fiscal regime that allows the U.S. to spend far more.

Consequences

Hanton is right to challenge some on the right, whose concern for mass immigration does not extend to foreign ownership of British capital. During Maggie’s tenure between 1979 and 1991, foreign ownership of British stocks never breached 13%. Now it is 60%. Thatcherism was built to deal with the challenges of a bloated, inefficient, but still significant, industrial great power. Today, Britain is still bloated and inefficient but is hollowed out and dominated by foreign capital.

Of course, foreign influence in Britain is far from limited to the U.S. The chair of the Conservative Party’s 1922 Committee, Bob Blackman, actively supports India’s incumbent BJP party and advocates for their interests in parliament. We have MPs who seem to care far more about either Israel or Palestine than domestic affairs. Our rich list is dominated by foreign oligarchs, most of whom are not American. Labour’s anti-corruption minister lost her office because of charges brought to her in Bangladesh. It seems right that if we fight the influence of a relatively benevolent Western hegemon, we’d question our general xenophilia at large.

Hanton’s remedies to U.S. dominance are not particularly strong. He calls for Britain to stop sell-offs and purchase golden shares in strategic champions. I am sympathetic to this, much to the chagrin of my Thatcherite coevals. But they do have a point about our track record in state development not being fantastic.

He says we should invest more in our people. To be honest, I don’t think this is a solution. The British elite believe in the power of education more than any other group on earth, as far as I can tell, and it does us precious little good. He also suggests we should do more research and development spending. This is all good, but big R&D budgets tend to come after the establishment of big conglomerates, not before.

Aside from this, there are one or two dubious statements. On page 128, he says, “Another demonstration of US success is the country’s trade surplus with Europe: annually, the US exports more than it imports.” Much to the dismay of American protectionists, the EU has a huge trade surplus in goods. After services and FDI, the EU still had a slight surplus in 2023.

Despite these quibbles, this is an interesting and punchy book that hopefully spurs a wider literature on foreign influence in Britain’s political economy.

Breathtaking