The lack of British 'Bigness'

It is time for Chesterfield Chaebols, Kidderminster Keiretsus, and Zone 6 Zaibatsus.

Go for growth. Time to Build. Build Back Better. Global Britain. The Green Industrial Revolution. Post-Covid economic discourse in the UK is centered around one central question. How do we avoid another decade of economic stasis? Despite its resonance among British policymakers, growth remains elusive. One of the key causes of this torpidity is the country’s historically low investment and the resulting lack of productivity gains. An important part of business investment is spending on research & development (R&D). Britain spends about 1.7% of its GDP on combined public and private R&D, compared to France’s 2.5%, Germany’s 3.1%, the U.S.’s 3.5%, South Korea’s 4.8%, and Israel's 5.4%. The government target is to get us to 2.4% by 2027: still lower than all comparable nations. Amazingly the target was set because it represented the OECD average. This shows the disconnect in British policy literature. Departments will breathlessly talk of the UK as a potential ‘science superpower’, only to set targets pegged towards the mean. Now, as fate would have it, the Office of National Statistics has gone and revised British business R&D spending estimates upwards by close to 50% due to a change in methodology. By the adjusted figures, the U.K. has met its 2.4% target and is hovering there right now. This is an enormous adjustment that could call a lot of government statistics into question. Treat with skepticism. Even assuming it is true, Britain would be at the OECD average in R&D spending and still lagging behind comparable nations. I will therefore press on with my argument. You can find a wonky thread explaining the change here.

There is solid literature diagnosing this problem. Richard Jones, a former physics professor at my old stomping ground in Sheffield, documents the UK’s R&D efforts brilliantly here. There are many ideas on how to fix the problem. First, there are direct increases in the government’s research budget. This is suitable, but inevitably begs the question: where is this money to come from? On the flip side of direct investment, there are calls for tax reform, usually centered around full expensing or making the largely unsuccessful super-deduction permanent. This too would be viable, but on its own would not be decisive. A 2019 Tax Foundation study finds Britain ranking 33rd out of 36 countries for its tax environment and 30th for machinery. But the study also found Germany at 32nd for machinery and Japan 34th overall. Yet both have an R&D intensity of over 3%. Full expensing or changing the planning system are important steps, but not determinative. Tax cuts in the short term would reduce government tax receipts: hindering increases in direct government research spending.

There is also immigration. America is highlighted as the primary example here. But as useful as high-skilled immigration is, it does not correlate heavily with R&D intensity. Korea, one of the top performers in R&D intensity, has an immigrant population of 2.3%. The large numbers of immigrant founders amongst America’s fortune 500 companies are primarily traced back to the nineteenth and early-twentieth centuries and owe just as much to America’s lack of established industries and enormous economies of scale. An increase in numbers, on top of an already very open system, is not likely to be transformative. In some cases, overreliance on gluts of low-skilled labor can deter investment in productivity-improving technologies or even reverse automation – as seen in the replacement of commercial car washing machines with cheap, off-the-books manual cleaners during the Cameron years.

Then, there are reforms around housing. That Cambridge and Oxford, the centers of British engineering excellence, do not build means very little lab space. The current allocation of government funds does not plan for this nimbyism and could be better allocated to fast-growing towns in Mercia. More ideally, governments would find ways to build in Oxford and Cambridge. The past government’s attempts at this were an unmitigated failure and were easily rebuffed. Some commentators argue for more agreeable reform via win-win mechanisms like Street Votes, the outcome of which we will see. Some proposals get closer to the problem by calling for new institutions, like a department of innovation. The fact that the UK’s semiconductor policy is co-developed by BEIS and DCMS is a sign of dysfunction. But these reforms are secondary. They neglect to acknowledge the primary limitation of the British investment landscape; the lack of research-intensive large companies in relevant industries.

Analysis

Looking at the top corporate R&D spenders, a pattern is clear. They are either gigantic tech platforms with monopoly status or manufacturing giants. They almost all have very strong connections with their respective governments. And very few of them are British. Based on 2020 EU data which I highly recommend you skim through, out of the top 2,500 corporate R&D spenders worldwide, 121 are British. Our biggest spender is GlaxoSmithKline, which ranks 29th. The total spending for these companies was €32 billion. For France, it was €34 billion, but with only 68 companies. For South Korea, it was €33 billion with 59 companies. €15 billion alone was funded by Samsung. For Germany: €87 billion from 124 companies. Based on this list of companies, the average R&D spend per company for the UK is way below other large economies. The average U.S. company spend was €449 million, for Germany it was €698 million, and for France, it was €497 million. For South Korea, it was €558 million and for Sweden, it was €315 million. For Britain, it was €265 million. Britain has a higher average spend than Denmark and Israel, as their companies are generally much smaller. That said, their companies are also centered in R&D-heavy industries and have greater investment intensity. Denmark’s Vestas is the world leader in wind power and the city of Odense is home to a dynamic robotics cluster. Israel has built a direct link between the expertise of its military and a burgeoning cybersecurity industry. So Britain is in the middle, poorly represented amongst technology platforms, industrial manufacturers, or small but innovative industries. We, therefore, have few huge R&D spenders, and a limited presence in small but R&D-intensive industries.

Of course, the UK does have its big companies, but they are generally focused on industries that are not research-intensive. HSBC has an R&D intensity of 3.6%: referring to the percentage of revenue allocated to R&D. For BP and Dutch Shell, it is 0.1% and 0.3% respectively. For Unilever, it is 1.6%. When the UK has contenders in an investment-heavy industry like pharmaceuticals, they invest plenty. British AstraZeneca had a higher R&D intensity than French Sanofi, German Bayer, American Johnson & Johnson, or Swiss Roche. This complicates the assertion that Britain’s drag in R&D is down to taxes or policy complications. Our primary problem is we lack the big agents in the right industries.

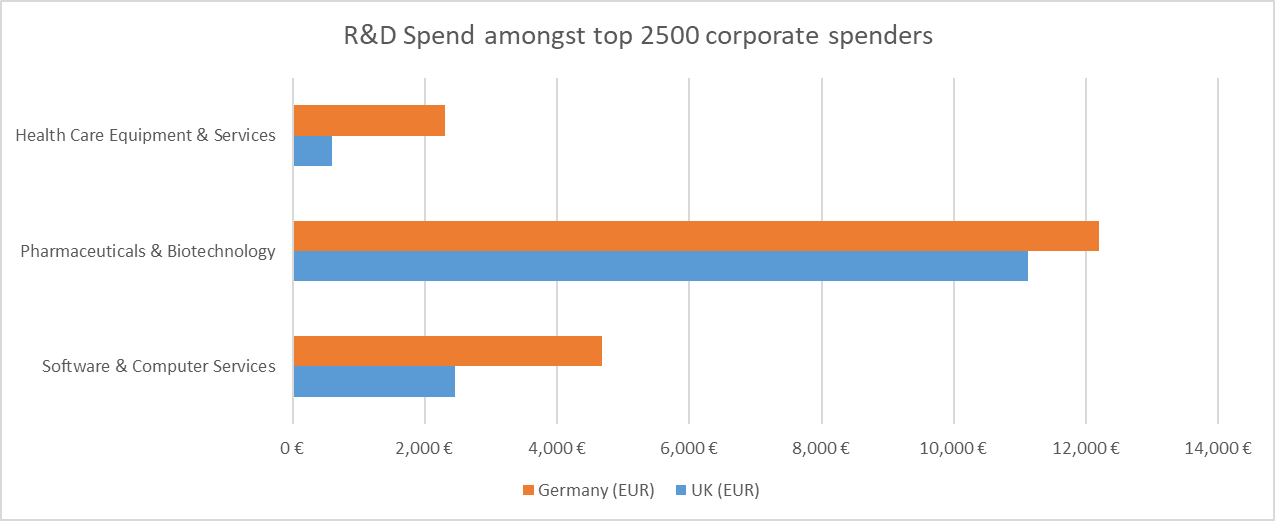

A comparison with Germany exemplifies this. A majority of German business R&D comes from 15 automobile companies: about €45 billion. Let us ignore this to even the two up. Take this central pillar of the economy away and German business R&D is still larger than Britain’s at €41 billion vs €32 billion. Broken down by segment, German firms invest more in industrial equipment, chemicals, and engineering. Ok sure, Germany is Europe’s premier manufacturer, but their computer and software services sector also invests a lot more than ours. Their pharmaceutical sector is more R&D intensive – despite having only 9 major pharmaceutical companies to the UK’s 20. This has less to do with intensity than it does with size. We also lag behind them in healthcare equipment & services. These sectors are mentioned as strengths in a recent paper discussing the UK’s comparative advantage in services.

Where does the UK spend more than Germany? Well, tobacco, oil & gas, aerospace & defence, banking, and financial services are the most notable. Tobacco is hardly the future. Oil & gas might last much longer as a sector than pundits realize, but is hardly fashionable. Aerospace & Defence, frankly, should not count as business spending since the only customers are governments. And while banks spending on R&D is good, is it not their job to facilitate other sectors to invest? A large banking sector does not correlate with more R&D spending. Another category is financial services, where we spend €224 million on R&D, compared to Germany’s €142 million. Other sectors include media, food & drug retailing, nonlife insurance, and food production. None of these sectors are R&D intensive. We are winning in the wrong places.

The UK is, therefore, hardwired for a comparatively low investment environment. Supply-side reforms cannot direct economic activity in R&D-intensive industries to the degree needed to make up the gap in funding. Catching up to advanced countries with 3%+ GDP investment will have to be met by increased government spending. This is in the context of an aging, debt-ridden society which doesn’t want to build but does want to double the defense budget. Now, these are just the 2500 biggest R&D spenders. SMEs are still important. There is some evidence that R&D spending by SMEs in the UK is undercounted. But we are lacking representatives in three major research constituencies;

Supersized Technology Platforms: The most profitable and highest valued companies in the world (including FAANG, Microsoft, and the Chinese BAT players). Very few countries beyond the U.S. and China have a presence in this space, but their sheer scale and/or profitability have made them big players in technology development. In virtually all cases, they receive enormous government support and are ring-fenced from the competition by market dynamics and geopolitical patronage. The UK has little prospect of attaining such a company.

Large Industrial manufacturers: Regionally and globally competitive companies with over £1 billion in revenue. Slow returns but high in investment and R&D. Often big employers.

Mid-to-large companies in smaller but relevant fields: The UK has its share of ‘unicorns’. More than any European competitor and fourth in the world. But while their valuations are enormous, many of these companies are hardly pushing the technological frontier. The remaining private ‘automotive’ company on the unicorn list, called Motorway, is an online-only used car marketplace. It seems UK VCs are drawn to a certain aesthetic pitch that projects ingenuity but is more often than not scraping the barrel of Web 2.0. We could use a few more robotics clusters like the one at Odense.

A case for a new industrial elite?

So we need a cadre of industrial giants to grow our R&D without breaking the government bank, but how do we get them? It starts with understanding how they are made and maintained. To a great extent, we had them. Imperial Chemical Industries (ICI) was the first UK company to make a profit of over £1 billion. The Marconi company, founded by Italian emigree Guglielmo Marconi, was the world’s first major telecommunications company. General Electric Corporation, also enjoying £1 billion in profits in the early nineties, botched a drive to telecommunications and was a victim of the Dot-Com bubble. Its CEO Lord Weinstock failed at the succession problem. The assets of these former champions have since been scattered across other British companies or in many cases foreign ones.

Here the issue of foreign ownership arises. British investors notoriously undervalue manufacturers with unremarkable but consistent returns, while foreigners are more than happy to gobble them up. U.S.-based Parker Hannifin’s attempted takeover of Meggit or the trading of Arm between International tech giants Softbank and Nvidia is a case in point. Some say we should not be worried. After all, foreign-owned firms are more productive than British ones. If all our big employers are foreign, who cares? This is after all how it is in Vietnam, where South Korea’s Samsung is the biggest employer. The Japanese carmaker Nissan’s plant in Sunderland was ranked Europe’s most productive in 2002, showing that Japanese production methods could be translated to the British workforce. This success might have implied that the British workforce was capable of building its own world-leading car companies. Instead, it affirmed that foreign companies are essentially better for the economy. Rather than an indicator of the potential of the British worker, it confirms the inferiority of our management class. To be nonchalant about foreign ownership of your industrial base is to resign Britain to being a perpetual consumer of someone else’s modernity. These companies will never prioritize British workers or towns if the incentives are not perfectly aligned, and their governments will not reciprocate British nonchalance about foreign ownership of key industries. Over-reliance on foreign ownership also tends to exacerbate current account deficits. Australia, which enjoys a healthy trade surplus, is nevertheless debt-ridden due to paying out royalties to foreign owners of equities and debt. Britain does not enjoy Australia’s key advantage: an abundance of commodities. Our account deficits, on top of the growing frequency of debt splurges caused by ever more frequent ‘seismic events’ like Covid, are only sustainable as long as the sterling is solid. This in turn requires continual foreign investment in the City, which in turn steers the economy away from industry and expands foreign ownership. There is growing evidence that speculators are losing confidence in the Sterling. If so, Britain’s economy suddenly looks a lot smaller. This problem can be summed up in the phrase ‘global Britain’. It projects insufferable neediness, an obsession with pleasing foreigners who are, understandably, predisposed to their interests. There is no push for a ‘global Ruhr industrial region’ or a ‘global Silicon Valley’ or a global South Korean Shipbuilding industry. Success speaks for itself. Volkswagen is part-owned by the state of Lower Saxony, and Samsung’s family is directly linked to the South Korean government. Or take the U.S., where Amazon, the country’s largest technology spender, hired Obama’s former head of public procurement. Biden has decided to keep ALL the trade restrictions bought in by the Trump administration. The American economy is becoming geared towards reindustrialization and reshoring. The more European countries stagnate demographically, the more jealously they will guard their trade surpluses. Free trade and openness about foreign ownership are losing their luster.

Industrial champions cannot be manufactured out of thin air. Though government investments and even national corporations could play a role, making this work requires at least a 10-year timeframe. The tradeoffs will be difficult. But one thing we could do is make it possible for company executives and enterprising families with dynastic ambitions to run their commercial operations through foundations. This is popular in Sweden, Denmark, and Germany: wealthy, technologically adept North European countries with many similarities to Britain, but who are richer and more investment-driven. Even France has enabled foundation ownership. It was only banned in the U.S. in 1969. Business foundations allow earnings to be stored away and be exempt from taxation. But they must recycle dividends into broadly defined philanthropic causes. This could be funding new cancer treatments or improving science-based education or just refurbishing an opera house. The philanthropic endeavors can often be a soft form of industrial policy. For instance, the Wallenberg family in Sweden funds the country’s largest private AI initiative through their foundation. They allow owners, particularly families, to avoid internecine feuds over who controls the wealth by placing it out of arms reach. As a result, foundation-run companies tend to last a very long time. The security and corporate coziness implied by this system can make companies less adventurous in the short term, but it also allows them the safety to invest in industries that are important but have long time horizons for returns. In effect, you are giving wealthy business owners security and the prospect of long-term status in the country, in exchange for them being less mercenary. Combine this incentive with some punitive measures on more egregious forms of tax avoidance, and we might lay the foundation for a business elite more aligned with the long-term economic prosperity of the UK. Any industrial strategy is a productive conspiracy between government bureaucracies and rich people. Any policy platform is secondary to this basic fact.

The answers to Britain’s economic woes won’t be found in a coworking space in Silicon Roundabout. Having large and globally competitive industrial companies is a standard that sets great economic nations apart from the rest. If you hope for any industrial strategy to succeed, it must be driven by companies that see themselves as distinctly British. It is time for Chesterfield Chaebols, Kidderminster Keiretsus, and Zone 6 Zaibatsus. It is time for Fomorian giants in Forest Green and Lovecraftian terrors in Lowestoft. Gogmaggogs in Guildford, Behemoths in Barnstaple, Grindylows in Grimsby and Leviathans in Leighton Buzzard. If we are to get back to Jerusalem, we should give the dark Satanic mills a chance.

Lord Weinstock also said "we do not innovate", in getting Marconi out of the semiconductor business, something my granddad (from the Elliott Automation side of the house) never let a day go by without quoting:-)

also I'd point out that historically even if the Ruhrgebiet or Korean shipbuilding didn't have a cringey slogan, they most definitely did have a conscious and explicit focus on export-led growth, to the detriment of other priorities. German industrialists saw exporting both as an opportunity and as a hedge against potential, then real, political conflict at home starting in the 1880s at least (the "exportventile" or export safety valve) and have never stopped. Similarly, if you open a textbook to the page marked "export-led growth" in the index you'll find a Korean case study, it's extremely well known that they set out to export a ton of tankers (not as if there was a huge, or any, home market).

The Valley is different because of being joined at the hip to the DOD and cold war big science, but there's probably an interesting story about the transition from being suppliers to IBM projects for the Feds to global exporting.