Reactive industrial policy

Britain is right to protect steel, but wrong to discover the need for protection only after domestic industry has already been hollowed out.

The UK government recently announced a set of increased trade protections on twenty categories of steel. The UK, since leaving the EU, has retained a tariff-plus-quota protection system for steel. Quotas of a certain tonnage are set for different product categories, and once that quota has been used up nationally, tariffs are incurred. The categories covered are:

1 Hot-rolled flat steel (coils, sheets, strips)

4 Galvanised and other metallic-coated sheet steel

5 Painted / plastic-coated sheet steel

6 Tinplate and packaging steel (food cans, beverage cans)

7 Heavy steel plate (quarto plate)

12A Alloy merchant bars and small structural sections

12B Carbon steel merchant bars and small structural sections

13 Reinforcing bar (”rebar”) for concrete

14 Stainless steel bars and light sections

15 Stainless steel wire rod

16 Carbon and alloy steel wire rod

17 Structural steel sections (angles, channels, beams, etc.)

19 Railway track products (rails and related material)

20 Gas line pipe

21 Hollow structural sections (square and rectangular tubes)

25A Large welded pipes (certain types)

25B Other large welded pipes

26 Other welded tubes and pipes

27 Cold-finished steel bars

28 Steel wire

From 1 July 2026, the quotas are being reduced 60%, and the tariff rate is being increased to 50%. This has led to a real pushback from the industries that use these categories of steel products, particularly construction and the advanced manufacturing sectors like automotive and aerospace.

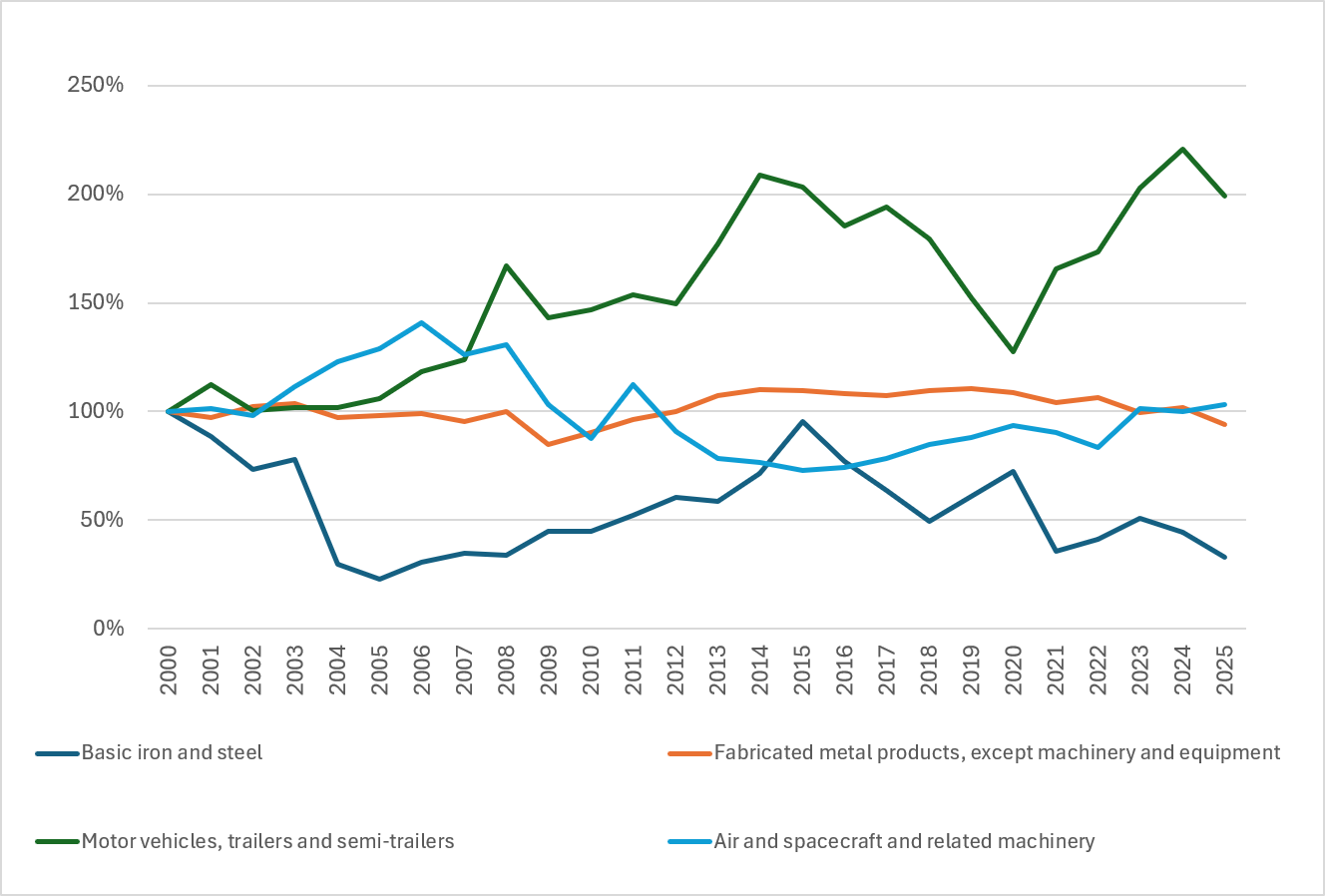

Below, we can see the difficult trajectory of British industry in the 21st century. The UK, since the late 90s, has run a very low protection, low-support regime on manufacturing, exposing it fully to the global market. Because British industry does not have the same number of well-capitalised industrial conglomerates as Germany, Denmark, Sweden, Japan or South Korea, we tend to have less vertical integration. What can be imported will be imported.

As we can see, up to 2008, this arrangement benefited discrete manufacturing industries like aerospace and automotive, while hurting heavy industry like basic steel manufacturing, and meant a stagnation in intermediate steel products (wire, pipes, tubes, components).

Figure 1: GVA output index for different manufacturing sectors (2000 = 100%). Source: ONS - GDP Low Level Aggregates 2025.

The promise of globalisation, shedding more basic manufacturing to specialise in higher-value-added sectors, seemed to be paying off.

But since 2008, air and spacecraft manufacturing has been down as well. Fabricated metal production recovered somewhat but has faltered recently, and after years of seemingly healthy growth, the automotive sector is now facing several existential challenges (outlined here).

No UK manufacturing sector is in particularly rude health. But basic iron and steel making is facing an existential crisis. Scunthorpe, though now nationalised, is struggling to produce much steel at all. Tata Steel is not making primary steel currently, as it shifts to an electric arc furnace (possibly delayed to 2028). Without tariff increases, there is a good chance that Tata will exit the market.

Tariffs, of course, put potential prices up for users of steel products. The consumers say adding to their costs imperils their own businesses. In some cases, these companies can only source speciality steel grades from foreign sources. Their costs are going to go up.

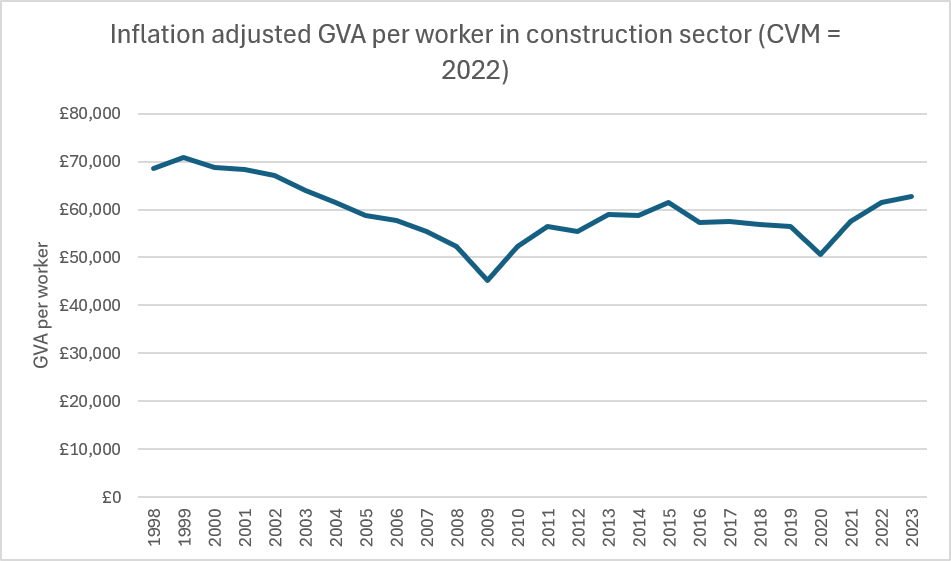

I would be less sympathetic towards the construction industry, which has said the tariffs would delay housebuilding. While manufacturers have manfully improved their productivity even in the face of stagnant growth, the construction industry has seen its productivity go into reverse during the 21st Century. The idea that a modest increase in steel prices will be the main barrier to it reaching any housing targets is dubious.

Figure 2: Construction industry productivity per worker. ONS workforce and GDP low-level aggregate tables.

It looks like the industry response has led the government to review its terms. We can therefore expect some category changes.

The trouble is, most major producers have implemented similar or more restrictive measures. The U..S. has succeeded in reducing foreign imports while modestly boosting domestic production. The EU and Canada have similar tariff-quota regimes to the UK. While users certainly have a case, without the tariffs, there is likely no long-term future for primary or secondary steelmaking in Britain.

I support nationalisation and upgrading at Scunthorpe on the basis that it’s strategically important to have domestic steelmaking capacity, and there is a strong likelihood that any gains in comparative advantage from the closure would be offset by Scunthorpe becoming a welfare desert. The possibility of merging British Steel with Liberty Speciality Steel’s EAF assets could be promising.

I am similarly sympathetic to the use of trade protections to counter global oversupply. It should be matched with demand-side stimulus in the form of procurement changes.

The deeper problem is not that the UK is protecting steel. It is that it is doing so after decades of allowing the domestic steel supply chain to weaken. Tariffs introduced when domestic mills are healthy can support investment. Tariffs introduced when plants are closing, capacity is constrained, and downstream users are import-dependent create chaos: they raise costs before the domestic alternative is ready.

A knee-jerk, crisis-induced industrial policy may be better than just passively letting British industry go belly up, but not by much.

It may take some time to heal from so many years, but it’s a necessary step forward.