How is U.S. manufacturing doing?

Checking in

Just a short one this week.

The Trump administration seeks to expand U.S. manufacturing and has adopted a relatively crude approach: imposing tariffs on imports and adopting a permissive regulatory stance domestically to stimulate production. How is it getting on?

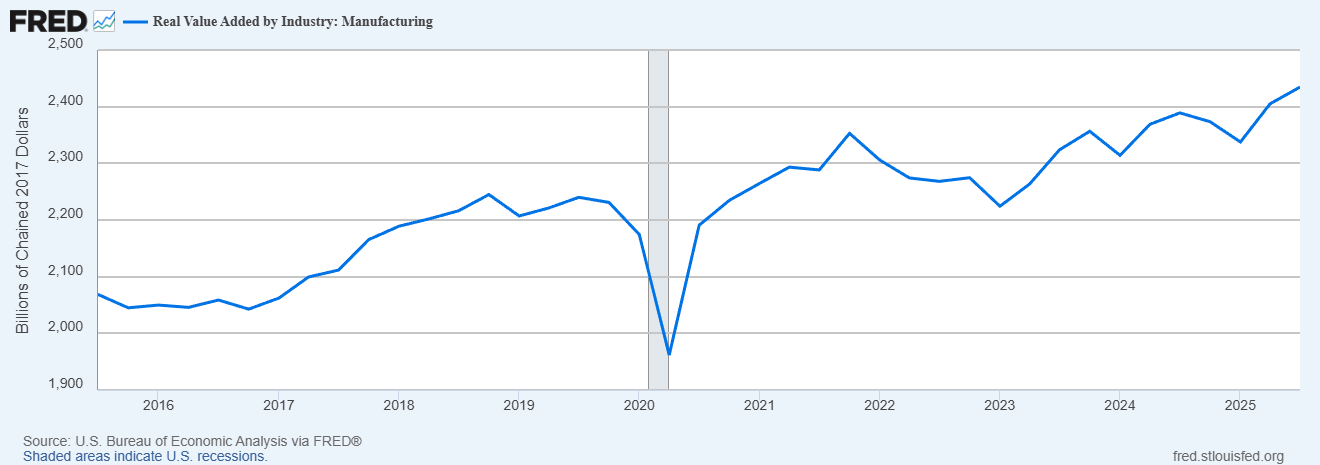

The big picture: U.S. manufacturing GVA (chained volume) is doing fairly well.

This could be due to some of the Biden stimulus starting to pay off. But, while manufacturing is not the main source of growth for Trump 2.0, it is looking healthy. This data will probably make his advisors think they can be more aggressive on tariffs without enormous blowback.

When looking at industrial production (a blend of economic indicators), the situation remains broadly positive.

This is not a manufacturing renaissance. Rather, there is a modest uptick.

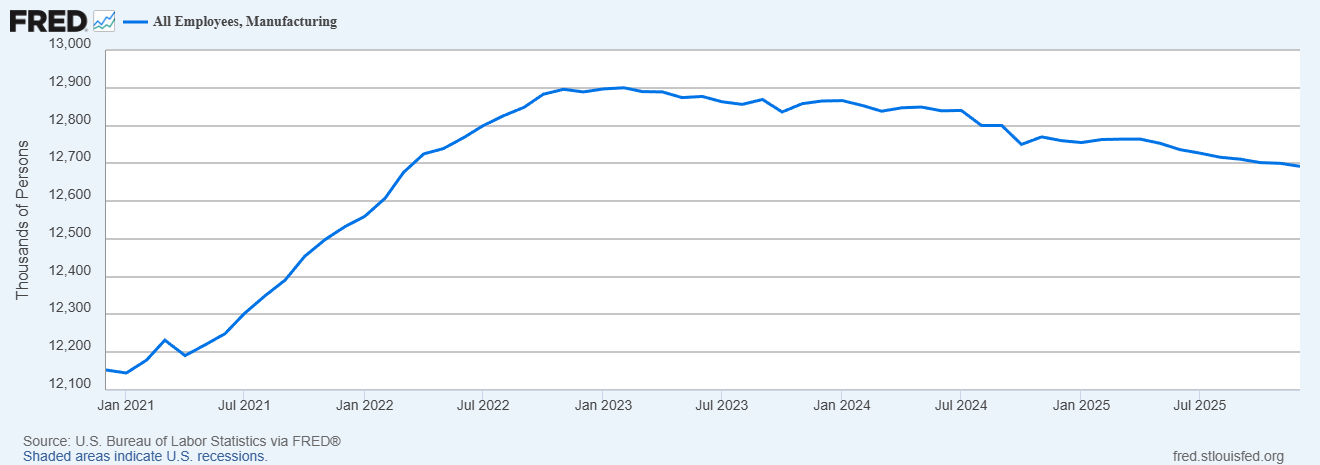

Employment has dropped somewhat, continuing a trend that began in 2022.

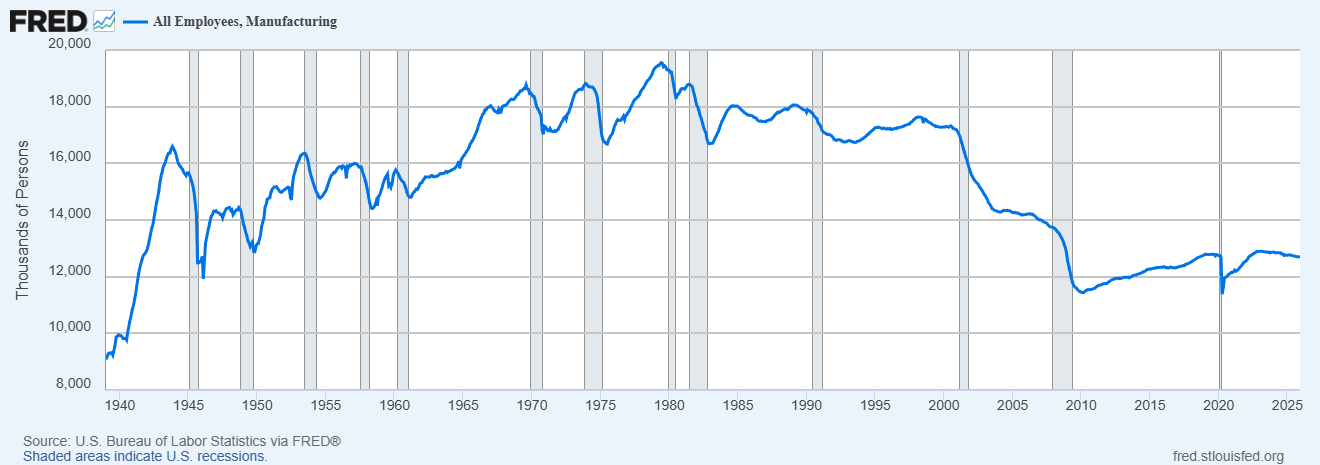

Looking further out, manufacturing employment has been pretty stable since 2010. The great loss of manufacturing jobs in America was limited to a fairly short period between 2000 and 2010. The obvious culprit is the China shock.

I think this is worth noting. Deindustrialisation is often described as a secular process, but in many cases, the massive declines in employment are short and sharp.

For specific sectors, the position is mixed. It was recently announced that U.S. steel production exceeded that of Japan for the first time in 26 years. It is worth noting that this is mainly due to Japan’s output declining and U.S. output remaining fairly stable. Tariffs from 2018 onwards probably helped this.

We can also see that U.S. import dependence for steel is declining, with output being fairly flat.

There is reason to believe the tariffs will provide some uplift to basic metal manufacturing in the U.S. Century Aluminium recently announced plans to build a smelter that would double domestic aluminium production. Whether the U.S. needs this, given its access to cheap Canadian and Icelandic aluminium, is another debate.

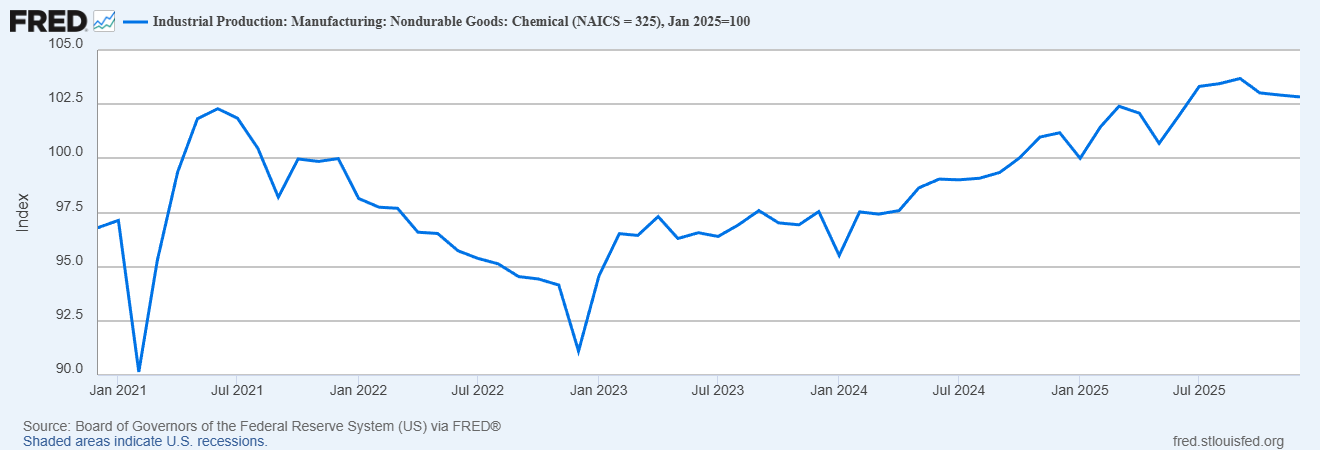

For chemicals, the picture seems rosy, but this is seen in long-term data. U.S. energy, especially natural gas, is cheaper than almost anywhere else, and this is evident in strong growth for energy-intensive sectors. Chemical production has grown markedly post-fracking. The relative rise in European prices has also helped.

2025 seems to continue that trend.

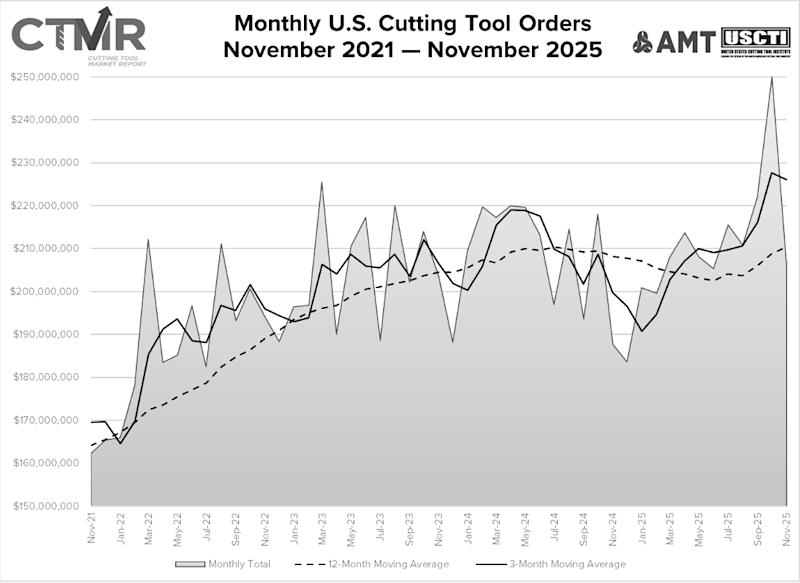

What about machine tools? Examining cutting tool orders, 2025 was astrong year for growth. Investment confidence seems reasonably high.

Other metrics are less edifying. Domestic auto production continues to decline, albeit at a slowing pace. This likely stems from the glut in global auto production.

While this gives only a fleeting picture, we can make some observations.

Although tariffs are a tax on consumption and harmful to individual manufacturers, they have not yet caused strategic harm to U.S. manufacturing. In fact, there has been modest growth.

While employment is declining, it is only at a trickle and comparable to the last few years.

Tariff-maxxers in the Trump admin, and maybe some Blue Dog Democrats, will look at the performance of manufacturing and feel relaxed about more interventions, tariffs and industrial policy, even if it is quite crude.

While manufacturing in the U.S. is not dying and is clearly in far better health than it was from 2008 to 2016, there is not yet much evidence of large-scale reindustrialisation comparable to that in China.

I would expect U.S. manufacturing capacity to be modestly to notably higher by 2028 than today, but at some cost to overall GDP growth, depending on how severe the tariffs remain. JD Vance, the likely Republican candidate and successor to Trump, would probably see this as a reasonable trade.

Securing a large market share in emerging industries such as batteries and drones is much harder than securing a strong position in established industries such as chemicals. The U.S. position here remains limited.

The Trump administration has, in my view, unnecessarily cultivated a lot of bad will in a short space of time. It will be interesting to see how much of a price manufacturers pay for this in 2026.

That is all.