Debrief 1: GKN and Melrose Industries

5 years after Melrose took over GKN, the future of its aerospace division is uncertain.

In this new series, I will cover a particular corporation, government agency, or institutional individual. I do something similar at Bismarck Analysis, but with a duty to cover a more comprehensive array of actors. Consider this an exercise in patriotic curiosity, with the aim of publishing shorter content more frequently.

First up, Melrose Industries, and in particular its 2018 acquisition, GKN.

Melrose was founded in 2005 by City veterans Simon Peckham, David Roper, and Christopher ‘Jock’ Miller. Peckham, now the company's Chief Executive, was formerly a solicitor and veteran of Walsall PLC, where he met Miller. He also worked in the equity finance division of the Royal Bank of Scotland between 2000 and 2003. Miller was formerly the Chief Executive of Walsall PLC. Roper had joined Peckham and Miller in setting up Melrose and was until 2020 the executive Vice Chairman. That position is now held by Miller.

Melrose is an industrial buyout firm headquartered in Birmingham. Its raison d’etre is buying out British industrial companies and selling them for a profit. It has an undeniable track record of quickly turning manufacturing businesses around and selling them for a significant profit. This has earned it a cult following within the City of London.

Melrose has bought and sold a number of companies, including;

McKechnie: Aerospace components.

Dynacast: Precision die-cast components. Sold to a U.S. consortium

FKI: A manufacturer of power generators.

Elster: German manufacturer of meters operating through three separate divisions with different markets and drivers (Gas, Electricity, Water). Sold to U.S. engineering giant Honeywell.

Nortek: Air management, security, home automation. Sold primarily to Chicago-based Madison Industries

All these have been reorganized and sold off, with shareholders getting between a 2X and 3X return on their original equity.

By far Melrose’s biggest acquisition was GKN in 2018 for £8.3 billion. Today it accounts for the vast majority of Melrose’s operations.

GKN is one of Britain’s oldest companies, tracing its origins back to Merthyr Tydfil during the Industrial Revolution. The initials refer to John Guest, Arthur Keen, and Joseph Henry Nettlefold, three industrialists who consolidated their respective steel mill operations around the turn of the 20th century.

GKN is revered for its age, having made cannonballs during the Napoleonic wars and a handful of Spitfires during WWII. Over the two world wars, GKN was largely centered around steel production but expanded into components for automobiles and aircraft. It moved away from pure steel production and into components from 1966 onwards. Since then, GKN has acquired a large number of other manufacturers. In 1994 it purchased the rotorcraft manufacturer, Westland, before selling to the Italian firm Leonardo. It also bought Focker Technologies, which traces its lineage back to the Dutch airplane designer Anthony Focker, the developer of some of Germany’s best-known fighter planes during the First World War. It is an old company with a venerable history, and Melrose’s acquisition courted a great deal of criticism.

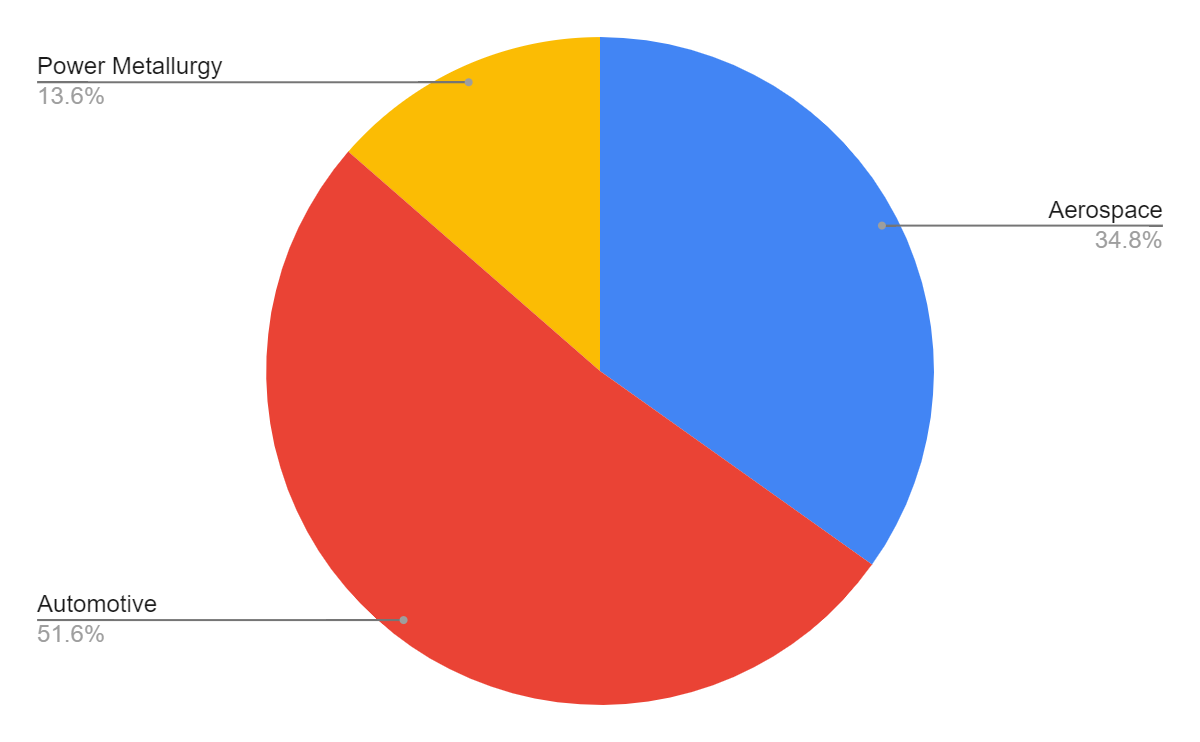

The company is primarily split between aerospace components and its automotive business. Its powder metallurgy business is something of a hidden jewel in the business.

Picture 1: GKN divisions by share of 2021 revenue, Source: Melrose Industries 2021 Financial Report

As can be seen below, the aerospace business is diversified, while the automotive and metallurgy businesses are relatively concentrated. Sintering takes up most of the metallurgy revenue. High-performance components generally need to use metals with very high-melting points, such as tungsten and Molybdenum, which need to be molded without being liquified. Sintering (using heat and pressure) achieves this. The nascent 3D-printing business is being headed up by veterans of large-scale foreign manufacturers like Jabil and Omron. Meanwhile, in automotive, most revenue is tied up in the manufacture of components for old-fashioned internal combustion engine (ICE) vehicles. A small but growing market is developing for electric vehicle components. For both automotive and metallurgy, there is real hope for new revenue streams in electric vehicles and additive manufacturing. These are far from mature yet, so there’s a real prospect for expanded revenue streams.

For aerospace, the picture is less optimistic. The division is already diversified between civil aircraft, engines, and defense procurement. Reports by the Teal Group for the next 10 years of the aerospace industry do not point towards a massive expansion in growth. While orders for single-aisle jet airliners will increase, orders for multi-aisle jetliners and regional liners will decrease. The U.S. military aerospace market is growing by virtue of the F-35, for which GKN is already supplying components. But the European defense market is projected to decline, as is the entire global market for rotorcraft (helicopters). In essence, there is not an immediate new growth market for an aerospace components supplier like GKN, and much of the high growth is located in China, where the business environment for defense-adjacent British businesses will only get worse.

Picture 2: Divisions and subdivisions of GKN (2021), Source: Melrose Industries 2021 Financial Report

The automotive and metallurgy arms are already in reasonable shape regarding profitability and will be split off into a separate company called Dowlais, which is set to be traded on the London Stock Exchange this year. The automotive division was consolidated in 2021 when the drivelines Erdington facility in Birmingham closed 2021, axing 500 production jobs and leaving just 50 white-collar jobs.

This leaves the aerospace business. An aerospace manufacturing facility in Kings Wood, Birmingham, was closed in 2021, costing 170 jobs. This decision was made formally by GKN aerospace management, rather than by Melrose. In 2018, they alleviated government concerns by stressing they would hold on to the aerospace division for at least five years. That time is nearly up.

Some of the opposition to Melrose’s takeover came from unions, including Unite. They even petitioned the former U.S. Defense Secretary ‘Mad Dog’ Mattis to intervene on the basis GKN supplies components for the F-35, arguing the takeover represented a threat to U.S. national security. But the move also attracted criticism from the UK trade association ADS. They argued the commitments provided by Melrose did not match the necessary investments needed for the lifecycle of new aircraft, meaning their manufacturers would be negatively impacted.

As for the government, much of the assurance it wanted was related to increasing pension provisions rather than national security, which Melrose happily obliged. There is a debate about how much the concerns were about national security, and how much they were about more anodyne ‘industrial policy’ goals like securing employment and promising investment.

Melrose’s binding commitment to hold onto GKN Aerospace is going to expire this year. The question now is who is going to be the new eventual owner? Melrose’s purchase came before the rollout of the 2021 National Security and Investment Act. The act makes defense-adjacent businesses like GKN Aerospace a less attractive prospect for potential buyers. The government can effectively block any sale on broadly defined ‘national security’ grounds.

This leaves a potential buyer pool of aerospace companies like Roll-Royce, a big Western defense contractor, or possibly a private equity group with sufficient funds to deal with the complexity brought on by new regulations.

Given the changing attitudes in government to intervention and the long-term tilt to expansive ‘industrial policy’, the Melrose takeover of GKN might be seen as a relic of a bygone consensus. In the meantime, however, its shareholders stand to enjoy considerable returns.