Carmageddon

Britain’s car industry faces a potential collapse

Last year, I wrote a short primer on Britain’s impressive but embattled automotive industrial base. A few months on, and the situation has become even more precarious. The portents are grim, the horses are chattering away, and the goat’s entrails are smelling funky. Carmageddon may be upon us.

State of play

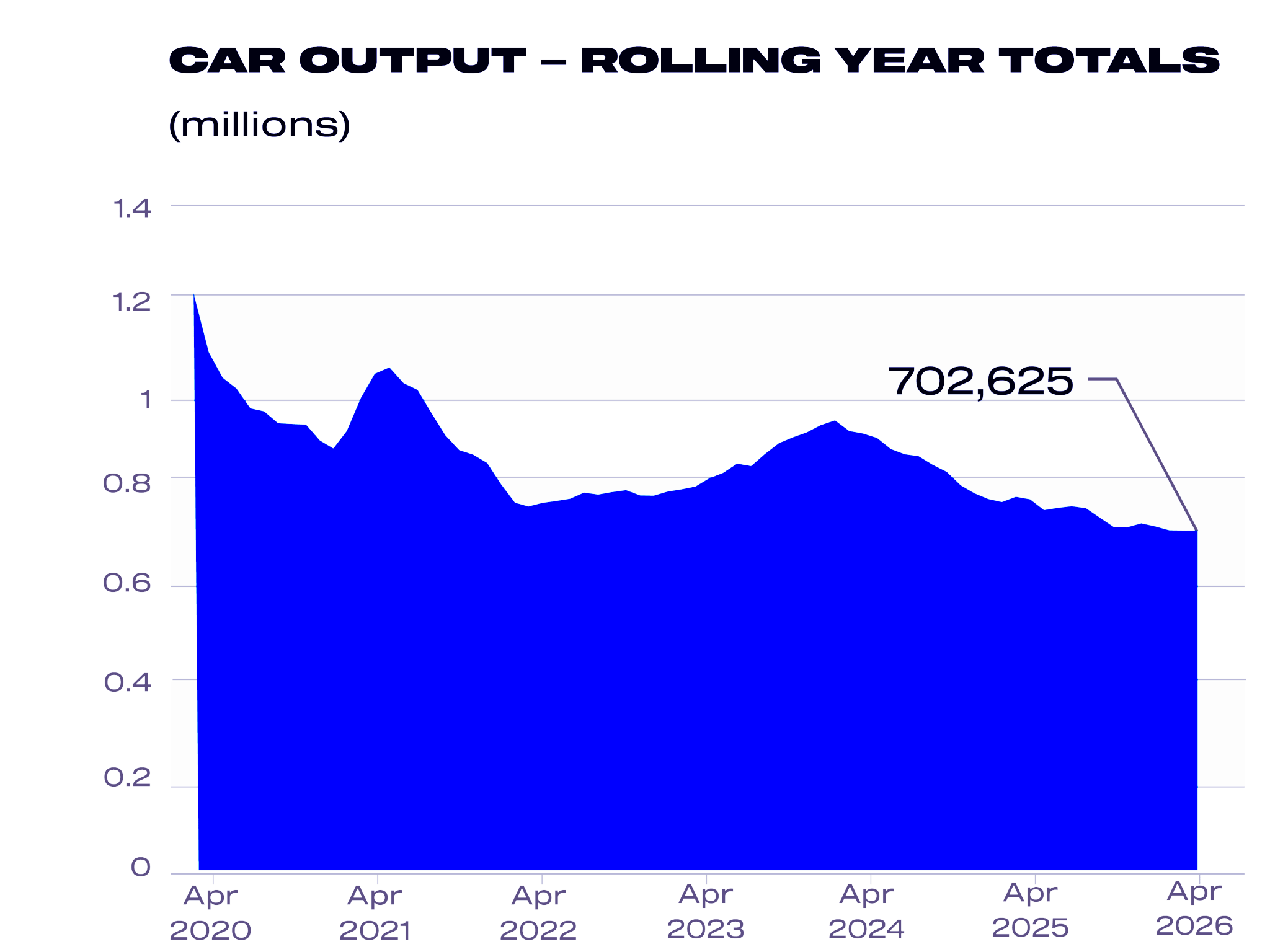

British car production is in a fragile state. A decade ago, the UK auto industry would have expected to manufacture around 1.5 million vehicles per year. In 2025, production fell to a record low of just 760,000 vehicles. Currently, 2026 is on course to be even worse. Car production up to May is down 10% YoY. Keep in mind that the government’s industrial policy aims to produce 1.3 million vehicles per year in 2035.

Figure 1: Rolling year totals for car output up to May 2026: Source: SMMT

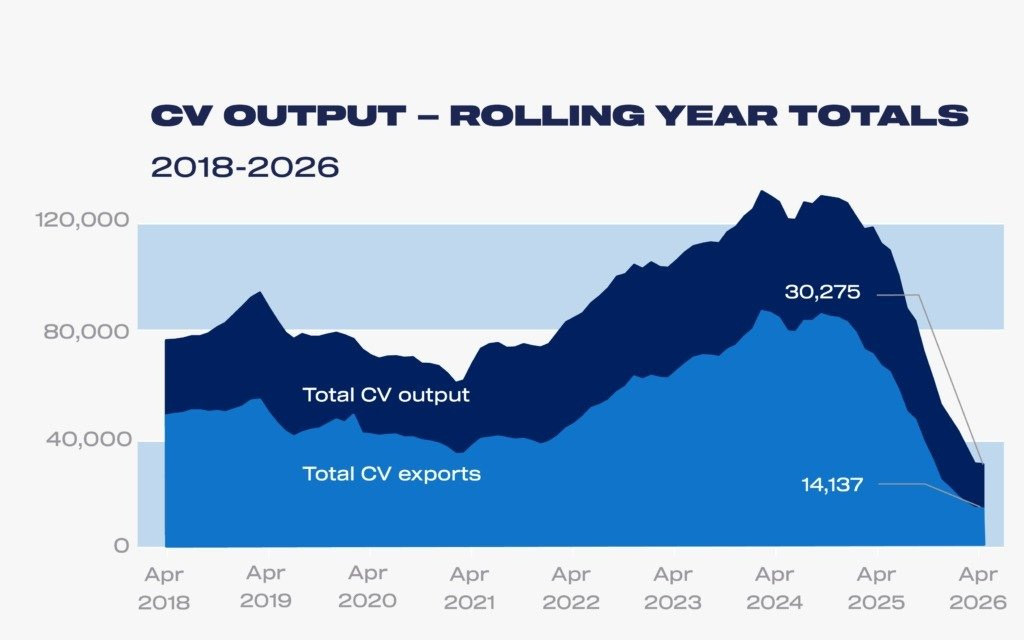

Meanwhile, the production of commercial vehicles (mainly vans) collapsed by 64% in 2025 from 126,000 in 2024 to 47,000, due to the closure of the Vauxhall plant in Luton. This drop will be somewhat offset in future years with Vauxhall owner Stellantis consolidating production at its Ellesmere Port facility on Merseyside. But the drop in production looks likely to be permanent.

Figure 2: Commercial vehicle output to April 2026. Source: SMMT

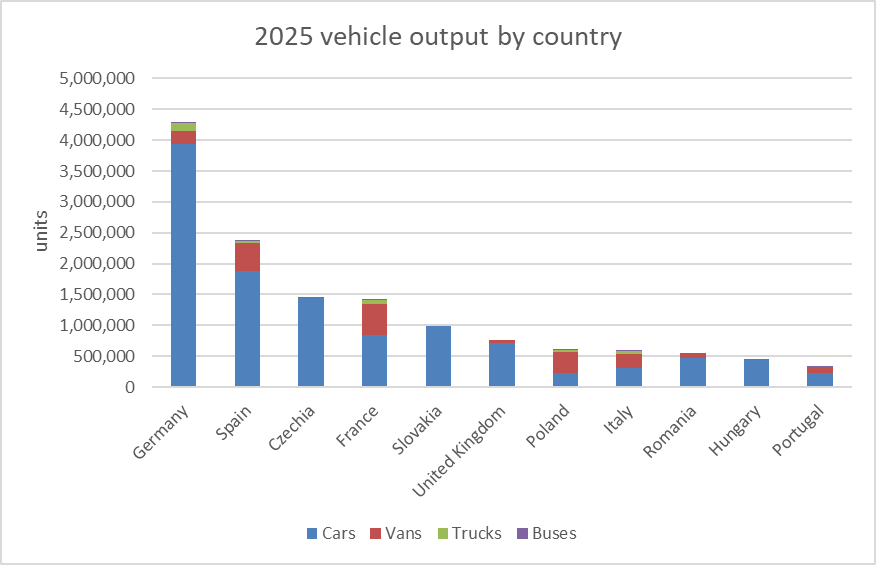

Britain is now the seventh largest vehicle producer in Europe and is likely just within the top twenty globally. We are not just behind Germany, Spain and France, but also Czechia and Slovakia. The chances are we will slip further down the table, because besides China, new auto factory investments are occurring in functional pro-industry Tier 2 economies like Poland, Hungary, Turkey, Morocco and Egypt. With so many countries targeting a slice of the global auto market, someone is going to lose out, and currently Britain is looking like a weak horse.

Figure 3: European vehicle output in 2025. Sources: OICA and SMMT

While talk of an imminent collapse might seem overly negative, the trendline is clearly alarming. The industry is also in a very precarious transition as it looks to shift fully to adopt battery-electric vehicles (BEVs) to accommodate the 2035 ban on internal combustion engine (ICE) vehicles.

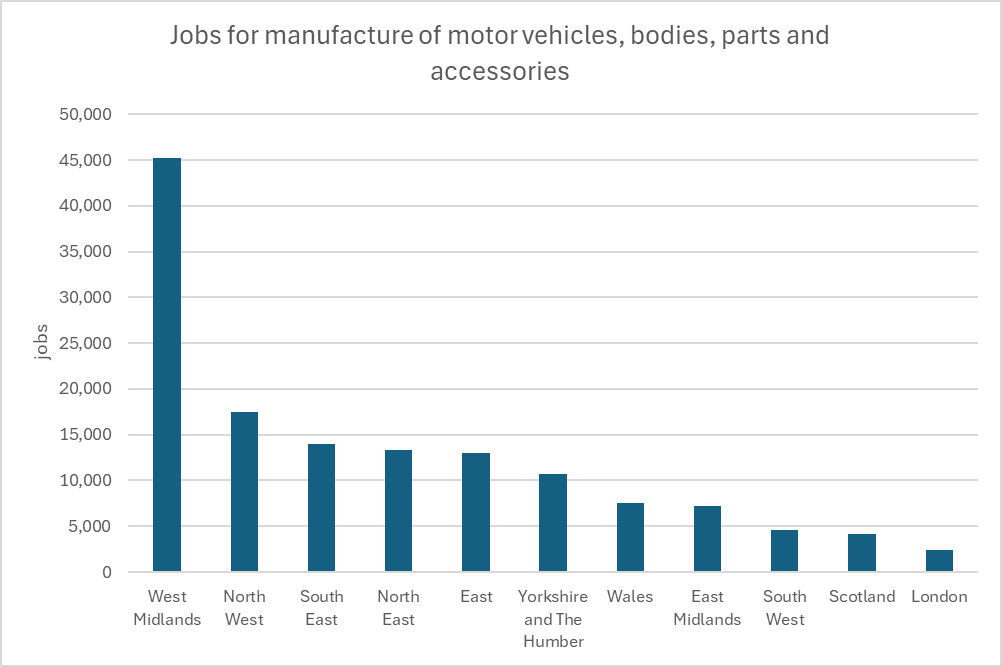

The British automotive sector, with a GVA of £18 billion, is nearly 10% of all manufacturing GVA. Besides its obvious economic value, its supply chain has dual importance for military productive capacity. It is geographically dominant in some of the most hotly contested constituencies. While the North West manufacturing base is more diversified with chemicals and pharmaceuticals, the West Midlands and North East industrial bases are dominated by automotive manufacturing. A government that allows it to collapse should not expect to last long.

Figure 4: Automotive manufacturing jobs by region. Source: NOMIS.

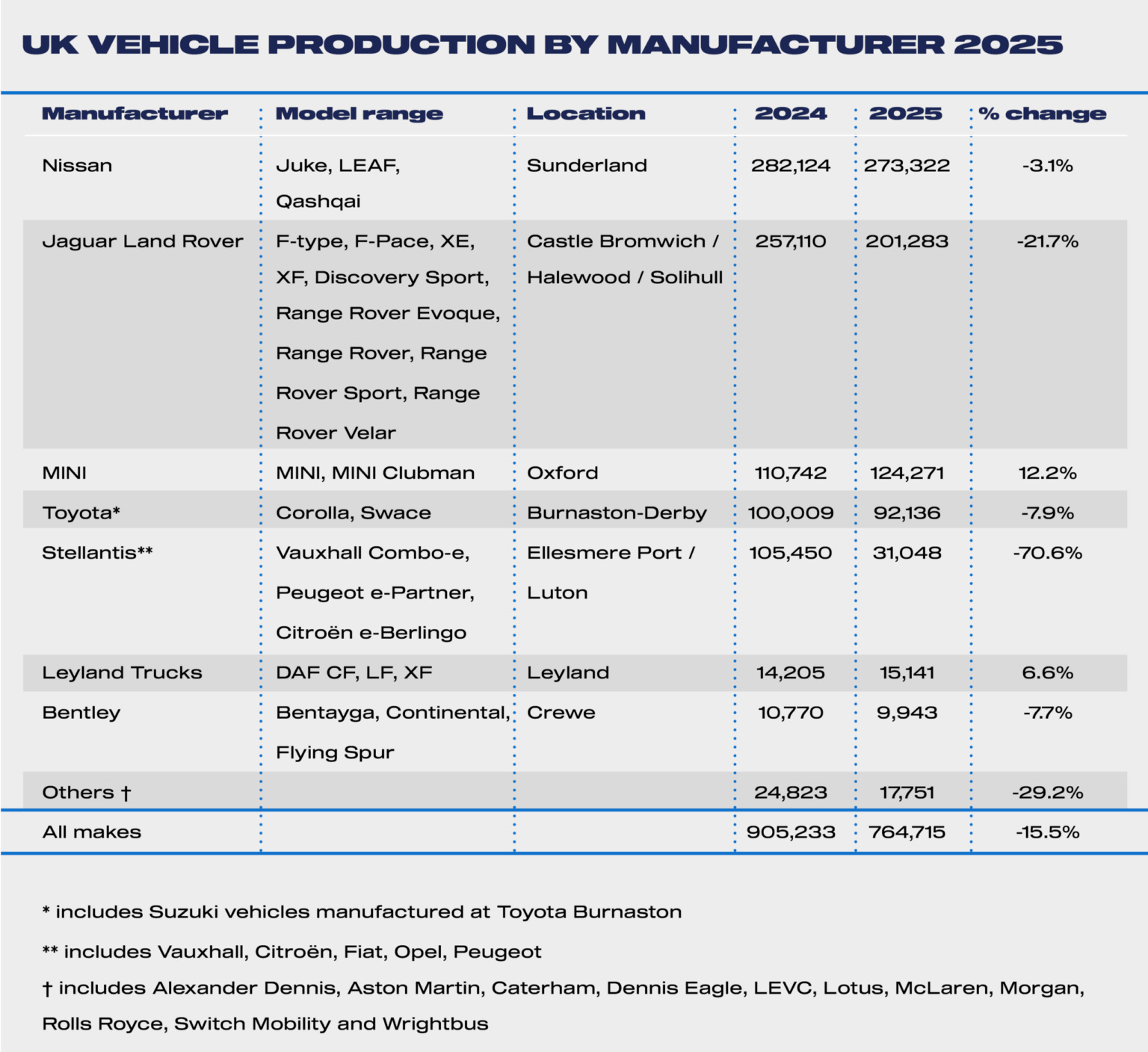

While British car production might at first seem very diverse and complex, it could be toppled by just a handful of executive meetings. These meetings would not take place in Britain, as the industry is, except for a few luxury brands, dominated by foreign conglomerates. There are but a small number of production clusters. The largest is Nissan’s plant in Sunderland. The primary ICE vehicles produced there are the Qashqai (the most popular domestically produced vehicle) and the Juke, with the LEAF electric vehicle restarting production in December 2025. This is currently the only BEV car being produced in Britain.

Figure 5: UK vehicle production by vendor and location. Source: SMMT

Then there is the West Midlands cluster, which is dominated by Jaguar Land Rover (JLR), owned by the Indian firm Tata Motors. Together, JLR and Nissan make up the majority of British car production. In the North West, there is the Stellantis Ellesmere Port complex, which mainly produces vans, with Leyland Trucks and Bentley close by. Toyota produces cars in South Derbyshire. There are then a handful of luxury car brands dispersed across the country. The luxury car category accounts for just 4% of vehicles, but around 12% of value.

Wider supply chain

All of these factories sit on top of an ecosystem of local suppliers who themselves are facing significant challenges.

Modern automotive supply chains are complex. There are a huge number of components in any car: upwards of 30,000 for modern vehicles. Among these components, there is a spectrum between low-value-to-weight components like body parts and high-value-to-weight components like semiconductors, with engines and batteries sitting somewhere in between.

Generally, the car body, chassis and major structural components are best supplied locally. Due to their weight, it is desirable to reduce transit costs and maintain immediate access to spare parts. This includes the bumpers, the headliners, tyres, wheel assemblies and large stamped body panels.

For sensors, electronics and harnesses, local production is less important than technical sophistication and economies of scale. In general, the higher the value-to-weight ratio, the less important local supply chains are. For this reason, the great bulk of electrical components in our cars are sourced from East Asia.

Britain has a very deep car body supply chain, a very small high-value components supply chain, and a very limited battery supply chain. We do, of course, have an extensive capacity for producing internal combustion engines, which will be shelved as we ban ICE cars in 2035.

What is meant by battery production? Essentially, raw materials are refined into chemicals and developed into cathode and anode materials, which are then used to manufacture battery cells. These processes are generally high-margin. After this, they are assembled into modules and/or battery packs, after which they can be integrated into vehicles. This section is less value-intensive.

Ideally, then, the production of cathode materials and battery cells is best off being integrated into the local supply chain, since it replaces the high-value manufacturing lost through the retirement of internal combustion engine (ICE) production. Of course, refining and manufacturing these batteries is energy-intensive and often dirty work, and so it is unsurprising that today’s battery manufacturing is dominated by China, with much of the remainder in Japan and South Korea.

Underutilisation threatens production

One of the big structural problems in the UK car industry is overcapacity and demand. Capacity utilisation in manufacturing should ideally run at above 80% to cover the fixed costs. From 2019 to 2023, Britain’s auto factory capacity utilisation fell from 65% to 54%. At Nissan’s plant in Sunderland, utilisation is currently below 50%.

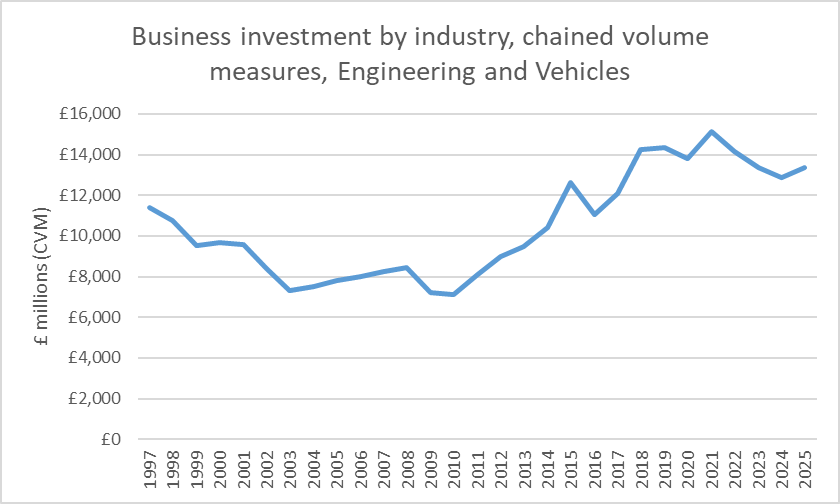

This obviously puts the economics of any car factory itself into question. Unit costs rise, volume declines, and the operations become less competitive. It becomes much harder to justify investments in capital equipment. After years of significant gains in business investment since 2008, there was a marked post-COVID slowdown in business investment.

Figure 6: Business investment in engineering and vehicles by year. Source: ONS

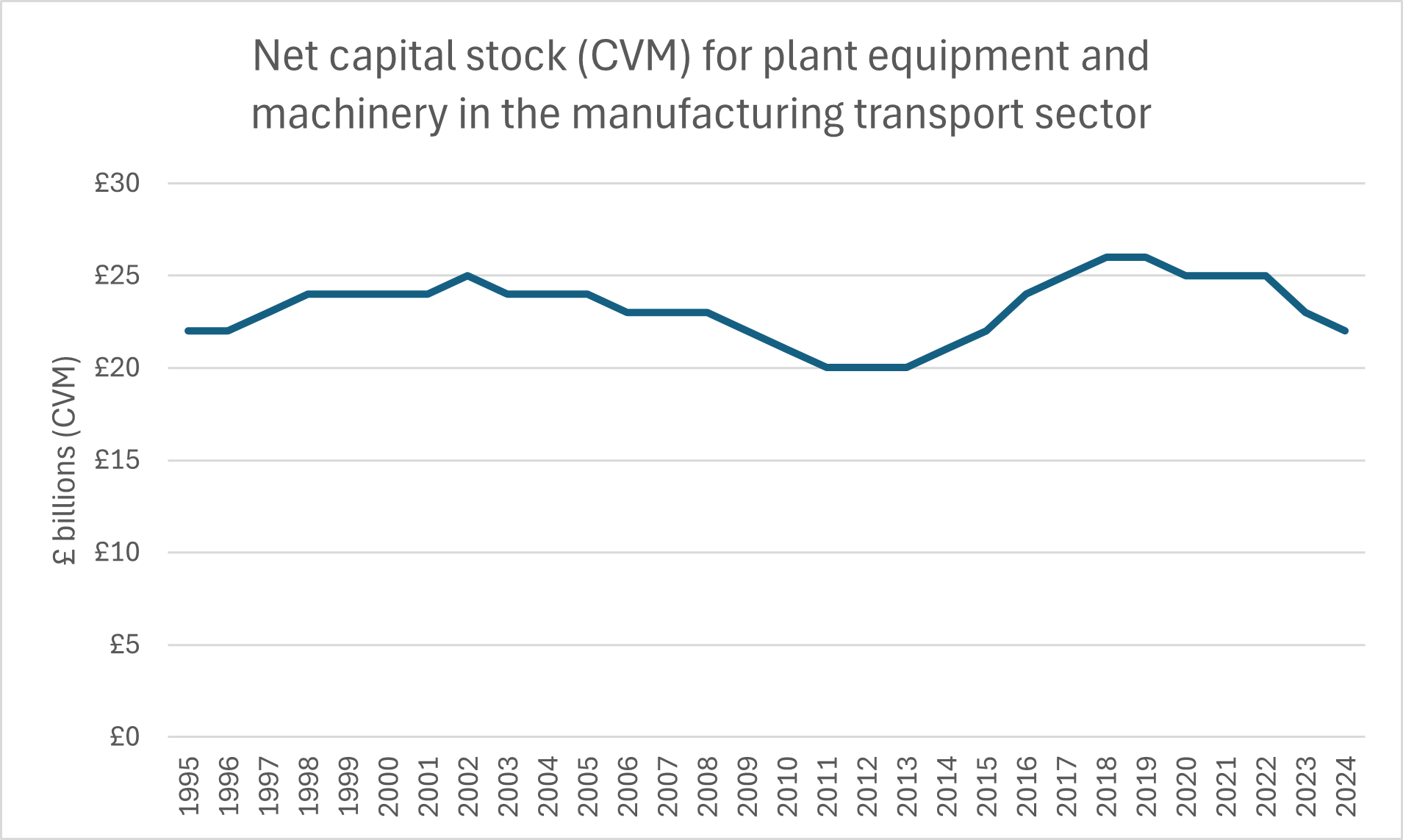

Despite investment having been substantial, the net capital stock of plant, machinery and equipment in our car plants is down from the levels it was in 1997. What investment boom there was in the immediate post-GFC era was not enough to set us up for future success.

Figure 7: Net capital stock for plant equipment and machinery in the manufacturing transport sector. Source: ONS

Besides the car manufacturers themselves, this lack of utilisation hurts the Tier 1 suppliers dotted around the factories. They cannot expect a steady stream of demand; their investment plans become more risk-averse, and their margins contract.

Such underutilisation and lack of obvious demand also make it very difficult to justify mega investments like gigafactory plants, which are needed to produce battery packs for BEVs. Some projects, like Britishvolt, have never materialised. Other projects, like Agratas in Somerset, need government grants to get over the line. This underutilisation is such an issue that it is leading manufacturers to consider partnerships once thought inconceivable (more below).

What is causing this underutilisation?

Electricity costs

Well, there is, of course, the cost of electricity and the cost of employment. Some would argue that automotive manufacturing is not particularly energy-intensive. This is true. According to a 2022 ONS survey, energy purchases relative to GVA were 2.7% for automotive manufacturing and 3.1% for car bodies. That said, the figure was double (6.1%) for accessories and car parts. Compared to steel, ceramics or refining, this is not very energy-intensive, but the figures would be significantly higher today than in 2019 due to higher energy input costs. And 2-6% can be a lot when margins are not particularly high for the car industry anyway. It is worth pointing out that battery production is quite energy-intensive, so if we anticipate electrification, we can expect electricity prices to be a serious concern.

When company heads and investors get into a room to decide where to place their factory, they are looking for the easiest metrics to compare each country. Few are as intuitive as energy costs, and it’s easy to find out just how expensive they are in Britain. Unless a country can offset high energy costs with very cheap labour costs or an abundance of capital equipment, which the UK cannot, the price per kWh may veto any investment in British industry. None of this is getting solved quickly. As Dieter Helm’s brilliant analysis points out, electricity prices are trending in the wrong direction for the next 15 years.

China and global overcapacity

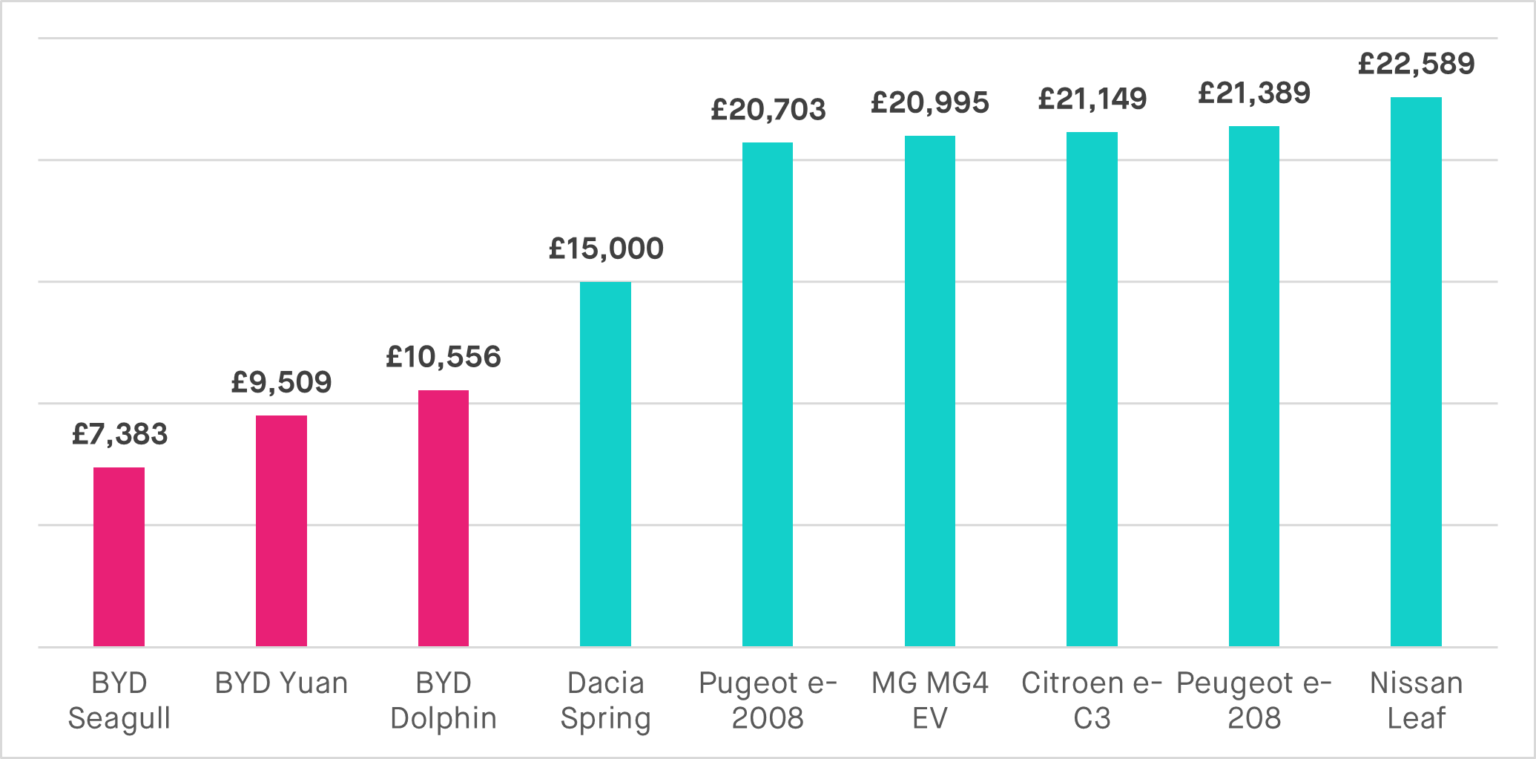

While Britain’s industrial malaise is likely deterring investment, a bigger problem is probably the massive downward pressure Chinese export growth is placing on global automotive production when global sales are stagnant. Chinese electric vehicles (EVs) also increasingly face tariffs elsewhere, and so the UK market is one of the truly open markets for their car exports. As we can see below, Chinese vehicles are much cheaper than domestic and European EV options.

Figure 8: Price differences for Chinese EVs vs UK models. Source: Social Market Foundation via Carwow and South China Morning Post.

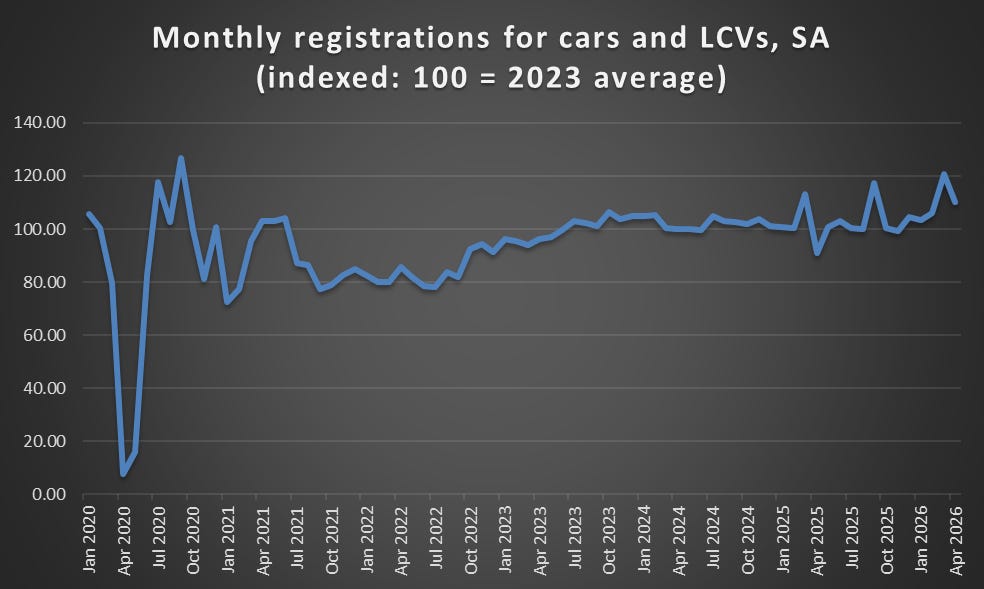

Were the number of new car registrations growing, there may be space for UK production and lots of imports to coexist, but registrations, as shown below, are not expanding rapidly.

Figure 9: New car registrations up to April 2026. Source: SMMT via ONS

Limited options to improve

The options to try and improve utilisation, then, are to make the industry more competitive at home. This is not easy as it requires investment, restructuring, and tough political battles regarding energy and taxes. Industry could get discounts for its electricity costs, and this could be passed on to consumers, who cannot easily leave en masse, but that is politically challenging.

Another option is tariffs. These have already been deployed in relation to steel, but for automotive manufacturing, it is trickier. For one, it is not broadly supported by industry. Any UK-based car manufacturer or Tier 1 supplier has had the opportunity to request the Trade Remedies Authority (TRA) to look into unfair trade practices, much as their European and American counterparts have. Not one request has been made. Why? China would retaliate, and 1% of the Chinese market means more than 10% of the UK market for the largely foreign owners of the UK automotive sector. Many of these companies are working in China through joint ventures and may very well hope to set up their future factories there. What is more, the luxury car market (Aston Martin, Bentley) relies heavily on the wealthy of Shenzhen and Shanghai.

EU Rules of Origin

Besides being in a poor position to implement tariffs, British car makers are expected to face incoming EU tariffs from 2027. These are the Rules of Origin requirements between the EU and the UK that were outlined in the 2021 Trade and Cooperation Agreement (TCA). The rules, originally intended to be implemented in 2024 but postponed to 2027, stipulate that electric cars can only be traded duty-free if at least 45% of their components are manufactured in the EU or the UK. For batteries, the threshold is even higher, at 60%.

More importantly, the cathode active material (CAM) will also have to come from within Europe or Britain, and currently, there is not enough to go around. There are only three major CAM producers in Europe, and their material is significantly more expensive than that of Chinese producers, even with a potential 10% tariff. Sam Lowe goes into this in more detail here.

UK–made vehicles that fail to meet the requirements will incur a 10% tariff from the EU. This is potentially very damaging, with 75% of our cars being for export and 55% of those being for the EU. There is also the prospect that the UK companies could miss out on subsidies provided by the EU, leading Nissan to say it may close the Sunderland plant.

The complications of the ZEV

These difficulties are occurring as British companies struggle to shift from producing ICE vehicles to BEVs. British and foreign manufacturers are, to varying degrees, losing money on the EVs they are selling here because the high cost associated with such vehicles is not being met by sufficient demand. Their ability to offset this with profitable sales of ICE vehicles and hybrids is constrained by the Zero Emission Vehicle (ZEV) mandate.

The ZEV mandate may seem simple. There is an annual target for BEV sales share, which, if not met, results in fines. But in reality, it is more complex. There are various “flexibilities” that can be used to bring down the “real” target below the stated one. As a result, some pro-ZEV think tanks have argued the mandate is actually on track. The flexibilities include:

Earning credits from the improved efficiency of non-BEVs.

Banking credits to use in the future or borrow against future performance.

Manufacturers trading credits with each other.

These efficiencies are not free. Borrowing credits means delaying the target, and trading means paying competitors.

In 2024, the ZEV car mandate was 22%, while the BEV market share was 19%. In 2025, the mandate was 28%, while the BEV share was 23%. In 2026, the mandate is 33%, and so far the BEV market share has been 23%. According to the think tank New Automotive, the real mandate, when taking into account flexibilities, for 2026, is 24%. It is clear that base ZEV targets are not being met, and fines are being avoided through flexibilities, which defer problems further down the line.

But even if fines are being avoided by car manufacturers, the industry still has to discount BEVs in order to get a sufficient uptick from consumers. According to SMMT, the industry has subsidised BEV purchases through discounts to the tune of £10 billion between 2024 and 2026, with the average discount for a BEV being around £11,000 per vehicle. There are notable spikes in BEV sales every December as companies race to avoid fines, even if it means taking losses on the sale. It is no surprise then that the industry bodies are supporting a review of the scheme, which is set to be released in 2027 (the industry wants this expedited).

Meanwhile, the similar ZEV mandate for vans is less equivocal - the target is not being met. In April 2026, 11% of van sales were zero-emission versus a headline target of 24%. The reasons for low adoption are many. Vans are utilised at high rates and do more mileage per day, making effective range when factoring in extra weight more of a consideration. Charging in the day can also hit businesses, often sole traders, very hard.

The single location for van manufacturing now is the Stellantis-owned plant in Ellesmere Port on Merseyside. It will exclusively manufacture BEV vans. The need to hit unrealistic targets could force them to discount their output, which in turn could lead to a full closure. While in the case of cars, manufacturers want to see more ZEV-related flexibilities, they are not calling for a full repeal. In the case of vans, the gap between the targets and uptake is an existential issue for future production.

Losing the capacity to build vans sends a terrible signal regarding the wider UK auto industry. Vans and other large form factors like trucks and pickups often have higher margins than passenger vehicles, and their supply chain is more closely linked with military production. The UK auto industry is rapidly becoming less capable in the range of vehicles it can manufacture.

While Starmer is pushing manufacturers to sell BEVs, Rachel Reeves is increasingly seeing the new fleet as a source of taxation. From 2026/27, BEVs will not be exempt from the vehicle excise duty. From 2028, BEV owners will also be charged a pay-per-mile electric vehicle excise duty. This shows the challenge of intervening in consumer choices in favour of a certain technology when the government’s purse relies heavily on taxing an established technology (ICE vehicles).

So to summarise:

UK car and CV production is hitting record lows

Van production fell over 60% in one year, and could end altogether

Investment growth has stalled, and the capital stock is declining

Existing plants are facing very low utilisation rates

Investor confidence is low, hurting potential battery production

Penetration of cheap Chinese BEVs is increasing, further hurting national production

The potential of EU and U.S. trade barriers is increasing

It is difficult for the UK car industry to envision setting tariffs on foreign imports without facing potentially existential backlash.

ZEV mandate and lack of demand are forcing companies to discount BEVs, deterring further investment and eating into margins.

A large-scale industrial collapse is quite possible – an event that would potentially destabilise a sitting government.

Where will UK Auto’s Tel Megiddo be?

So how might this collapse start? There are three potential areas of weakness. The car factories themselves, the wider supply chain, or the much-vaunted battery plants. If these are closed down, delayed further or cancelled, they could create a chain reaction whereby they take a large number of businesses with them. Since there are only a handful of automotive clusters in the UK, mass closures at one cluster could spill over into others very quickly.

The best bet may be in Oxfordshire, where the BMW-owned Oxford Mini plant still operates, producing over 100,000 ICE Minis per year. UK-based Mini EV production was supposed to come to Oxford in 2026, but that was put on hold in early 2025. BMW even refused a £60 million government grant to keep the project on track. Meanwhile, in China, they have entered into a joint venture with local firm Great Wall Motor to produce Mini EVs there. Additional Mini EVs are being produced in Leipzig, Saxony. These potential imports face no tariffs and benefit fully from the UK’s electric car grant for consumers.

So Mini EVs produced in China are undercutting the non-existent Mini EV offering in Britain. It begs the question, why would anyone bother to make Minis here?

It is hard not to see the paused decision in 2025 as the first step towards closure, with BMW executives pondering this very decision as we speak. One thing to keep in mind is that while companies, of course, want to make all their plants profitable, when the prospect of closures arises, one plant management team in one country will ruthlessly lobby against a counterpart in another jurisdiction. If the choice comes between the Leipzig plant and the Oxford plant, we can expect only one winner.

This would be a disaster of epic proportions, given the Mini is the second most produced UK vehicle and export model. Immediately, about 1/7th of the total production would be gone, creating cascading effects across suppliers up and down the country.

But this is just one area of potential weakness. A plant closure could just as easily be decided by the fall of a major local supplier. An anonymous source relayed to me that a major international car manufacturer with a British plant is buying components from local UK suppliers for its car production in Eastern Europe, despite the local European industrial base being perfectly adequate to supply itself. They are doing this because if the relevant UK suppliers didn’t have the foreign business, they would collapse, therefore imperilling the company’s own UK assembly line.

The last major threat is that battery plants essential to a transition to electric vehicles do not materialise in sufficient capacity or are cancelled. In October, I mentioned that the UK had very little battery-producing capacity. In 2012, the company AESC built a Sunderland plant, with 1.9 GWh of annual battery capacity. Since then, in late 2025, AESC opened another production line at the plant with 15.8 GWh in capacity. The new capacity gives Nissan a roadmap to scale up BEV production, even if it is likely to lose money on these models.

The next expected gigafactory is the Agratas plant in Somerset. With an expected capacity of up to 40 GWh, it will primarily supply JLR’s electric vehicle range. Originally scheduled for 2025, the Agratas plant has suffered multiple delays and is now projected to begin production by the end of 2027. To keep the project going, it needed £380 million in grants from the UK government in April 2026. Part of the reason for the delay has been JLR delaying the rollout of its EV range in order for demand to pick up.

In 2025, Tata, the owner of Agratas, sold a 12% stake in the company to AESC, the current UK gigafactory operator in Sunderland. AESC is itself headquartered in Japan but is owned by China’s Envision Group. China therefore now has an enormous stake in the battery plant infrastructure in Britain, leading to concerns about diversification.

There is still plenty of opportunity for the Agratas project to go belly up, but even if it gets built, this and the AESC plant in Sunderland do not get Britain the battery-manufacturing capacity necessary to produce over 1 million BEVs a year. Of course, Britain could import the batteries, as they would be cheaper. But then we would lose much of the product’s value, likely reducing the industry’s long-term gross value added. Without new commitments, imports rising, and the ZEV tightening, company executives could easily decide the UK is just not the place to build cars anymore.

The government tacitly accepts that there is a major risk of an industry collapse. It has provided a funding scheme called Drive35, which will distribute £2.5 billion in grants, loans and R&D support up to 2035 in order to provide ballast to the largest clusters. While very welcome, this will not offset a major downturn.

The Chinese to the rescue?

Ironically, it could be China’s auto industry that stops, or at least defers, Carmageddon.

In early June, Nissan signed a memorandum of understanding with the Chinese auto giant Chery, the maker of the Jaecoo and Omoda brands, to build vehicles at the Sunderland plant. While details are scarce and the deal is not over the line, this is clearly an attempt by Nissan executives to increase the plant’s sub-50% utilisation rate.

Becoming a contract manufacturer for Chinese companies is high on the government’s own agenda, and civil servants have reportedly been trying to get JLR to also build Chery vehicles. But this brings up some questions. How will these vehicles pass the rules of origin requirements to avoid potential EU sanctions? And how much of the local supply chain would benefit from the building of Chinese vehicles?

The likely first answer is that these vehicles will only be sold in the UK and will be essential for reaching the ZEV mandate. The second answer is likely that, in the event the deal goes through, the cars will be knock-down kits. This means Nissan would be importing ready-made kits filled with imported components, which are then assembled in Britain. From then on, gradually, the local supply chain *might* be permitted to get more involved.

This is already happening elsewhere. In 2024, Chery combined with a Spanish consortium to build knock-down kits in Catalonia. Stellantis was building EVs for the Chinese manufacturer in Poland, but it seems it is now moving production to Spain, perhaps because Poland has been more hawkish on Chinese trade practices.

But while this is happening in other countries, British producers are in a uniquely poor position to negotiate demands for higher domestic content. We have no potential tariff threat, and our utilisation rate is so poor that the mere threat of the Chinese walking away from investment could close whole factories.

This is late-stage British industrial policy. Rather than deal with systemic issues, we see companies bend over backwards to assemble Chinese-made kits to keep the factories just about open, so that we might fulfil a government mandate on electric vehicle registrations. We will likely go from having a highly complex auto industrial base that can manufacture vehicles of all types to an assembler of Chinese kits, with very little commercial vehicle production. Where once developed countries gave China the chance to assemble their products to save a few quid, now the Chinese will let us assemble their kits for market access – so that we might temporarily avoid factory closures.

This might just stave off Carmageddon and might keep some jobs. But it is a permanent downgrade from what we once had.

A depressing read.